India’s solar revolution is entering a new phase. For more than a decade, the country’s renewable energy expansion was shaped largely by government targets, reverse auctions, viability-gap support, renewable purchase obligations and large utility-scale projects backed by policy momentum. But a different pattern is now emerging beneath the surface. Increasingly, the next wave of solar growth is being pulled not merely by policy ambition, but by a rapidly changing electricity economy.

The shift is subtle but profound. Data centres, artificial intelligence infrastructure, green hydrogen projects, commercial consumers, middle-class rooftop adopters and energy-intensive industries are beginning to reshape the logic of India’s solar expansion. The transition is slowly becoming demand-led rather than policy-led — a development that could fundamentally alter investment patterns, grid planning, manufacturing priorities and even the political economy of electricity in India.

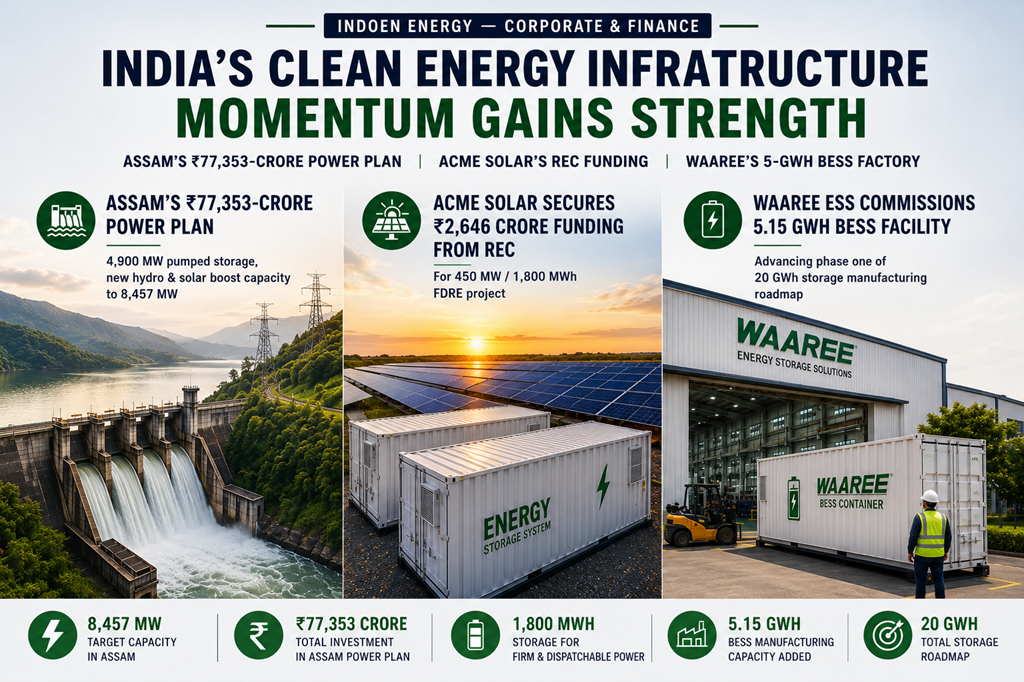

Recent developments across the sector reveal this transformation with unusual clarity. India’s solar sector attracted Rs 20,641 (US$2.19 billion) crore in foreign direct investment during financial year 2024-25 despite a broader slowdown in overall energy-sector FDI, signalling that investors continue to see long-term growth potential in solar-linked infrastructure and manufacturing.

At the same time, Gujarat-based Solex Energy announced plans for a 5 GW solar cell manufacturing facility alongside a 10 GW battery energy storage system unit, reflecting the industry’s growing focus on integrated energy ecosystems rather than standalone module production. Meanwhile, developers participating in the 6 GW Bikaner-V transmission project have reportedly shown reluctance to exit despite mounting challenges, underscoring how transmission infrastructure is becoming central to the next stage of renewable growth.

Coal India, historically associated with thermal energy dominance, has also commissioned a 100 MW solar project in Gujarat, illustrating how even legacy fossil-fuel institutions are repositioning themselves within the changing energy landscape.

What ties these otherwise separate developments together is the growing realisation that India’s electricity demand profile itself is changing faster than expected.

Data centres and AI are reshaping solar demand

One of the clearest drivers of this shift is the explosive rise of data centres and AI-linked digital infrastructure. India’s data centre capacity has expanded rapidly in recent years and is expected to multiply several times over by the end of the decade as artificial intelligence, cloud computing, fintech and digital public infrastructure scale up across the economy.

According to government data, India’s data centre capacity has already risen from roughly 375 MW in 2020 to nearly 1,500 MW by 2025. Several industry projections now suggest that installed data-centre capacity could rise to between 8 GW and 10 GW by 2030.

Unlike traditional industrial loads, modern data centres demand uninterrupted, high-quality electricity round the clock. This is pushing operators towards renewable-linked procurement models, hybrid renewable systems and battery-backed power arrangements.

Increasingly, solar energy is no longer being viewed only as a decarbonisation tool, but as a strategic hedge against volatile power costs and future energy insecurity.

Gujarat’s growing interest in becoming a data-centre hub reflects this new dynamic. Industry observers have pointed to the state’s relatively strong power infrastructure, land availability and renewable energy ecosystem as key advantages for future AI and cloud-computing investments.

Internationally, similar trends are becoming visible across major economies. The International Energy Agency and several global consultancies have warned that AI-driven data-centre growth could significantly reshape global electricity demand patterns by 2030.

In this context, India’s renewable expansion is increasingly being linked not just to climate goals, but to digital competitiveness itself.

Green hydrogen and storage are changing the economics of solar

This is where the nature of India’s solar growth begins to change. Earlier phases of expansion depended heavily on government auctions and central procurement agencies. Today, however, electricity-intensive sectors are beginning to create their own renewable demand independently of direct state intervention.

Green hydrogen is another major catalyst. Several analysts expect green hydrogen production, fertiliser decarbonisation and industrial electrification to become major sources of additional solar demand from the late 2020s onward. A recent industry assessment suggested that emerging sectors such as data centres and green hydrogen alone could drive an additional 15–20 GW of solar demand annually from FY29.

That would represent a structural transformation in India’s electricity market rather than a temporary surge. Such demand growth is already influencing corporate strategy.

The Solex Energy announcement involving both solar-cell manufacturing and battery storage manufacturing reflects how companies are preparing for a future where dispatchability and energy reliability matter as much as installed renewable capacity.

In many ways, storage is becoming the bridge between India’s solar ambitions and the operational realities of a digital, industrial and AI-driven economy.

Globally, the renewable sector is witnessing a similar evolution. Solar-heavy systems in Europe, China and parts of the United States are increasingly moving towards storage-linked flexibility models as daytime renewable surpluses collide with evening demand peaks.

India appears to be entering the early stages of that same transition, though with its own distinct characteristics shaped by industrialisation, urbanisation and digital expansion.

Rooftop solar is socialising the transition

At the same time, India’s solar growth is no longer confined to large corporate or utility-scale projects. Rooftop solar adoption among middle-class households is beginning to create a more decentralised and socially embedded energy transition.

The rapid expansion of schemes such as PM Surya Ghar has contributed to a visible increase in residential solar adoption across multiple states.

The economic logic is straightforward: rising electricity tariffs, declining solar-system costs and concerns about future power reliability are pushing households towards partial energy self-sufficiency. Rooftop solar is increasingly being viewed not merely as an environmental decision, but as a long-term household financial strategy.

This socialisation of solar may eventually prove politically significant. Once households begin producing electricity themselves, the relationship between consumers and distribution companies changes fundamentally.

Utilities in several regions have already begun expressing concerns about grid management, evening peak demand and revenue implications linked to widespread rooftop solar adoption. Experts, however, argue that such tensions largely reflect inadequate grid modernisation rather than inherent flaws in distributed solar systems.

The challenge, therefore, is increasingly shifting from generation capacity to system integration.

Transmission and grid integration may become the next bottleneck

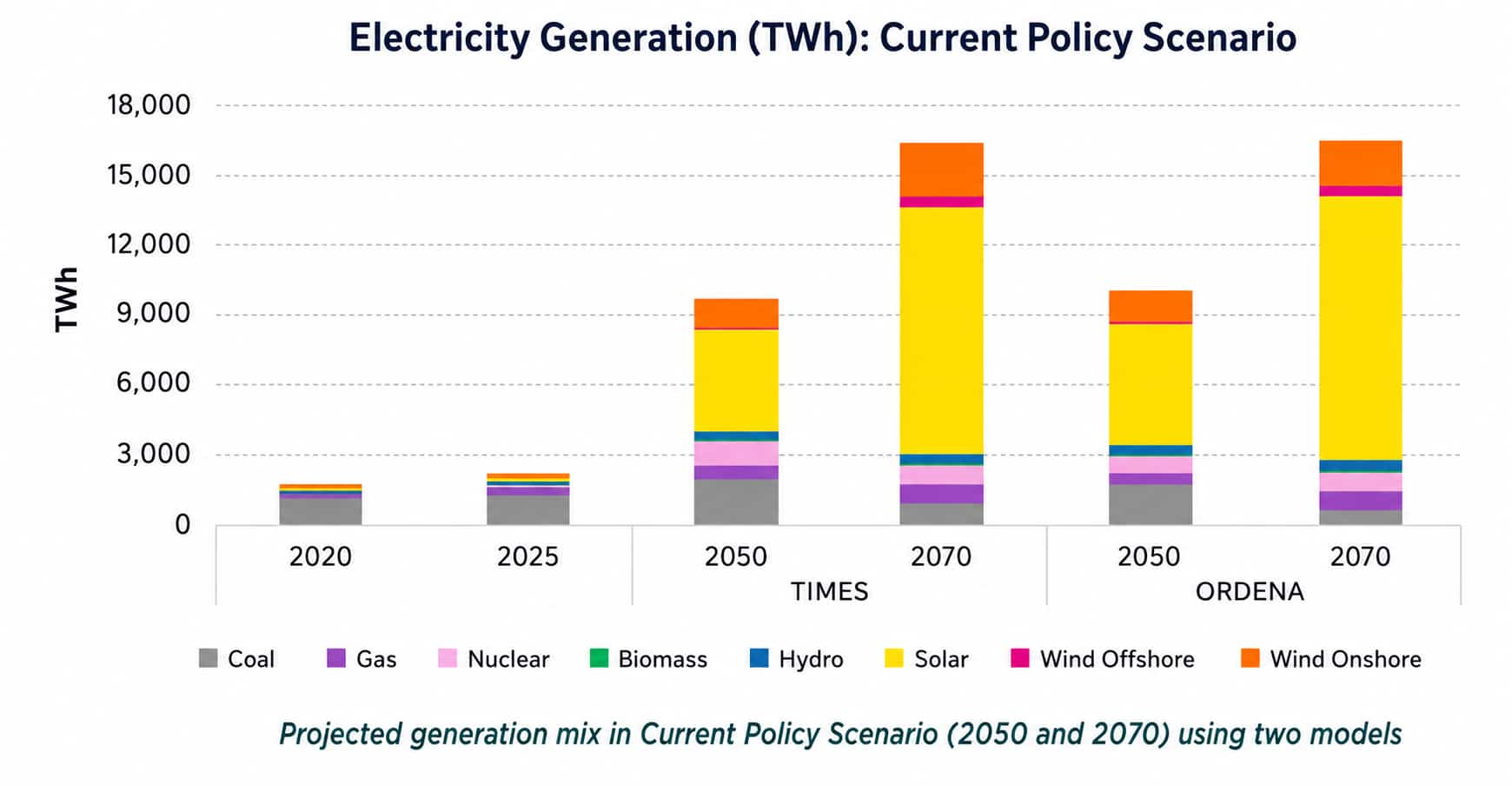

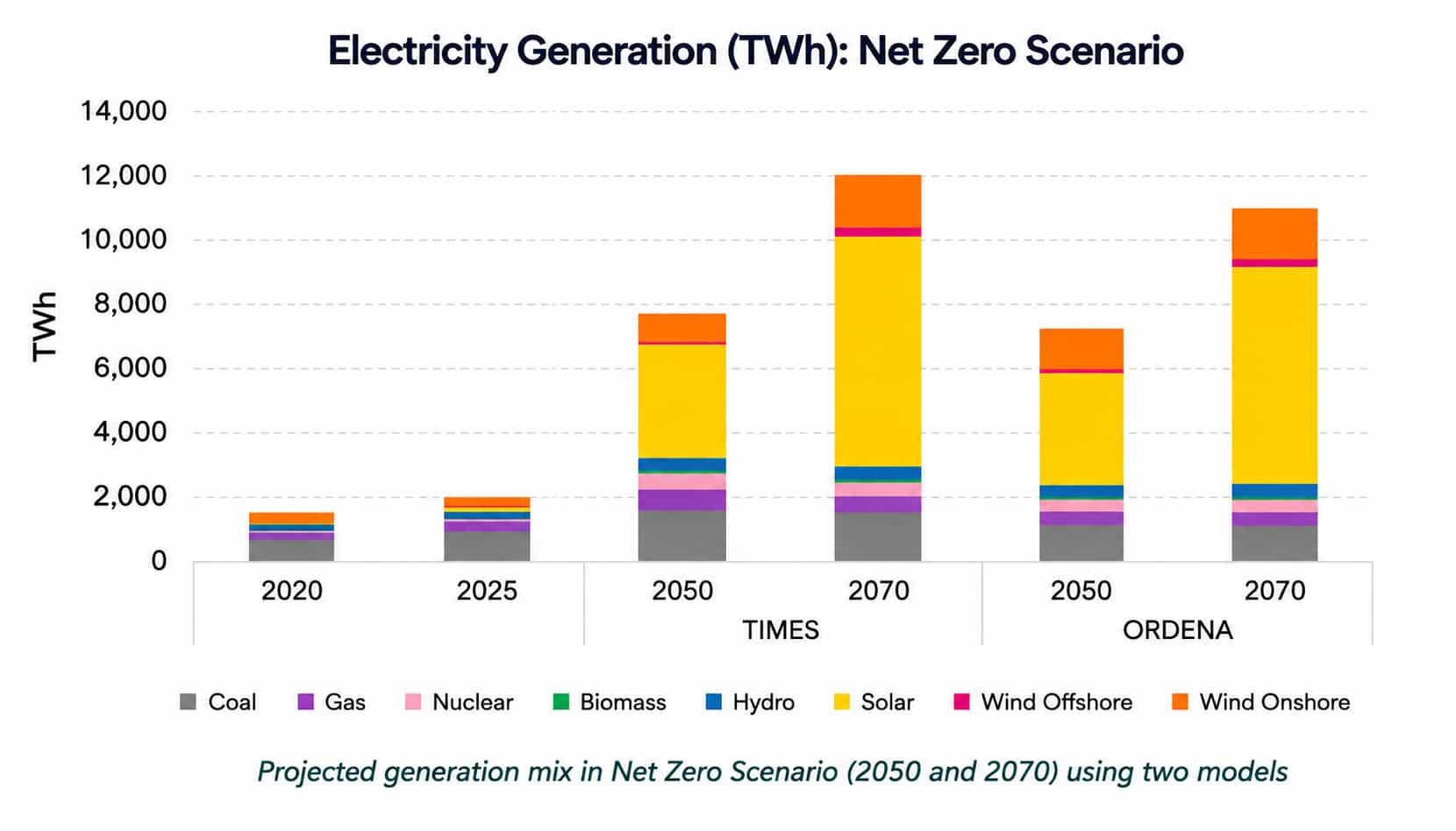

India has already crossed major renewable milestones.

The country added a record 50.9 GW of renewable capacity in FY26, including 44.6 GW of solar additions. Total non-fossil installed capacity has crossed 283 GW, placing India among the world’s leading renewable markets. But generation growth alone does not automatically translate into grid stability or reliable power delivery.

Transmission infrastructure is now emerging as one of the most critical bottlenecks in India’s energy transition. The concerns surrounding the Bikaner-V transmission project highlight how evacuation infrastructure, financing uncertainty and execution delays may increasingly shape the economics of renewable expansion.

A senior executive at a renewable infrastructure firm, speaking on condition of anonymity, said the sector is entering a “less glamorous but more difficult phase” of transition. “Adding solar capacity is no longer the only challenge,” the executive said.

“The next decade will depend on whether India can synchronise generation, storage, transmission and industrial demand growth together.”

This broader structural shift is also altering the role of conventional energy companies. Coal India’s commissioning of a solar project in Gujarat is not merely symbolic diversification. It reflects a deeper recognition within the sector that future electricity demand growth may increasingly favour renewable-linked assets even as thermal generation remains important for baseload support.

Indeed, India’s transition remains complex and far from linear. Coal continues to dominate electricity generation, accounting for over 70 per cent of power production. Rising electricity demand linked to urbanisation, manufacturing and extreme weather events is also forcing policymakers to maintain thermal capacity additions alongside renewable expansion.

This creates an important counterargument to overly optimistic renewable narratives.

Some analysts caution that India’s growing power demand may temporarily strengthen coal dependence even as renewable installations accelerate. Data centres, AI infrastructure and green hydrogen facilities require reliable round-the-clock electricity that current renewable-storage systems may not yet fully provide at scale.

However, this apparent contradiction may actually explain why battery storage, flexible grids and hybrid renewable systems are now attracting increasing attention. States such as Maharashtra have already introduced ambitious renewable-storage obligations and integrated energy-storage targets.

Another critical dimension is manufacturing localisation. India’s renewable sector is increasingly being linked to industrial policy, supply-chain security and geopolitical strategy.

The push for domestic solar-cell manufacturing, battery production and clean-energy supply chains is partly aimed at reducing dependence on imported components, particularly from China. Foreign investors appear to recognise this opportunity despite broader uncertainty in global clean-energy markets.

The continuing inflow of capital into India’s solar ecosystem suggests that global investors see the country not only as a renewable deployment market, but also as a long-term industrial platform.

This matters because the future of India’s solar transition may ultimately depend less on megawatt targets and more on whether the country can build a complete electricity ecosystem capable of supporting new forms of demand.

That ecosystem is becoming increasingly multidimensional. AI expansion is raising electricity intensity. Green hydrogen could reshape industrial power consumption. Rooftop solar is decentralising generation. Storage systems are becoming economically strategic. Transmission corridors are turning into critical infrastructure assets. Even geopolitical competition around manufacturing is beginning to intersect with renewable deployment.

In many ways, India’s energy transition is starting to resemble transformations already unfolding globally, where electricity itself is becoming the central organising force of industrial and digital economies.

The implications extend beyond the power sector. A demand-led renewable transition could reshape capital allocation, urban development, industrial policy and labour markets. States capable of offering reliable renewable-linked electricity may emerge as preferred destinations for data centres, AI infrastructure and future manufacturing clusters.

India’s solar transition, therefore, is no longer merely a climate story or an infrastructure story. It is increasingly becoming a story about economic architecture itself.

The next phase of growth may not be determined primarily by how many solar parks are announced each year. Instead, it may depend on whether India can build an electricity system sophisticated enough to power an AI economy, support industrial decarbonisation, manage decentralised generation and maintain affordability simultaneously.

That is a far more demanding challenge than simply adding renewable capacity. But it is also what makes the current phase of India’s solar transition far more consequential than the one that came before.