India’s banking sector is beginning to wake up to climate risk. But the country’s largest lenders still appear to be treating the issue more as a compliance obligation than a fundamental threat to financial stability, asset quality and long-term profitability.

That mismatch could become costly.

As extreme weather events intensify, supply chains fragment, coal assets risk becoming stranded, and regulators tighten climate-related supervision, the banking system is increasingly being pushed into unfamiliar territory. Floods, heatwaves and droughts are no longer distant environmental concerns; they are emerging credit risks.

A recent assessment by Climate Risk Horizons, paints a troubling picture of a sector making incremental progress in disclosures while lagging badly in substantive risk integration. Climate Risk Horizons

The timing is significant.

Globally, financial regulators are moving rapidly from climate ‘awareness’ to climate enforcement. Central banks in Europe are already penalising banks for inadequate climate preparedness.

The European Central Bank (ECB) recently imposed its first climate-risk-related fine on Spain’s Abanca for missing supervisory deadlines tied to climate-risk assessment frameworks. At the same time, the ECB has begun integrating climate factors into collateral frameworks, potentially lowering the value of carbon-intensive assets during refinancing operations.

India is now inching toward a similar direction.

The Reserve Bank of India has identified climate risk as a potential systemic threat and has introduced the RBI Climate Risk Information System (RB-CRIS) to improve access to climate-related financial data. The government, meanwhile, has released a draft climate finance taxonomy aimed at guiding investments toward climate-supportive and transition activities. SEBI has tightened ESG disclosure frameworks and introduced new rules governing sustainability-linked debt instruments.

Yet beneath these regulatory developments lies a stark reality: most Indian banks are still unprepared for the scale of the transition ahead.

The climate threat is becoming economic reality

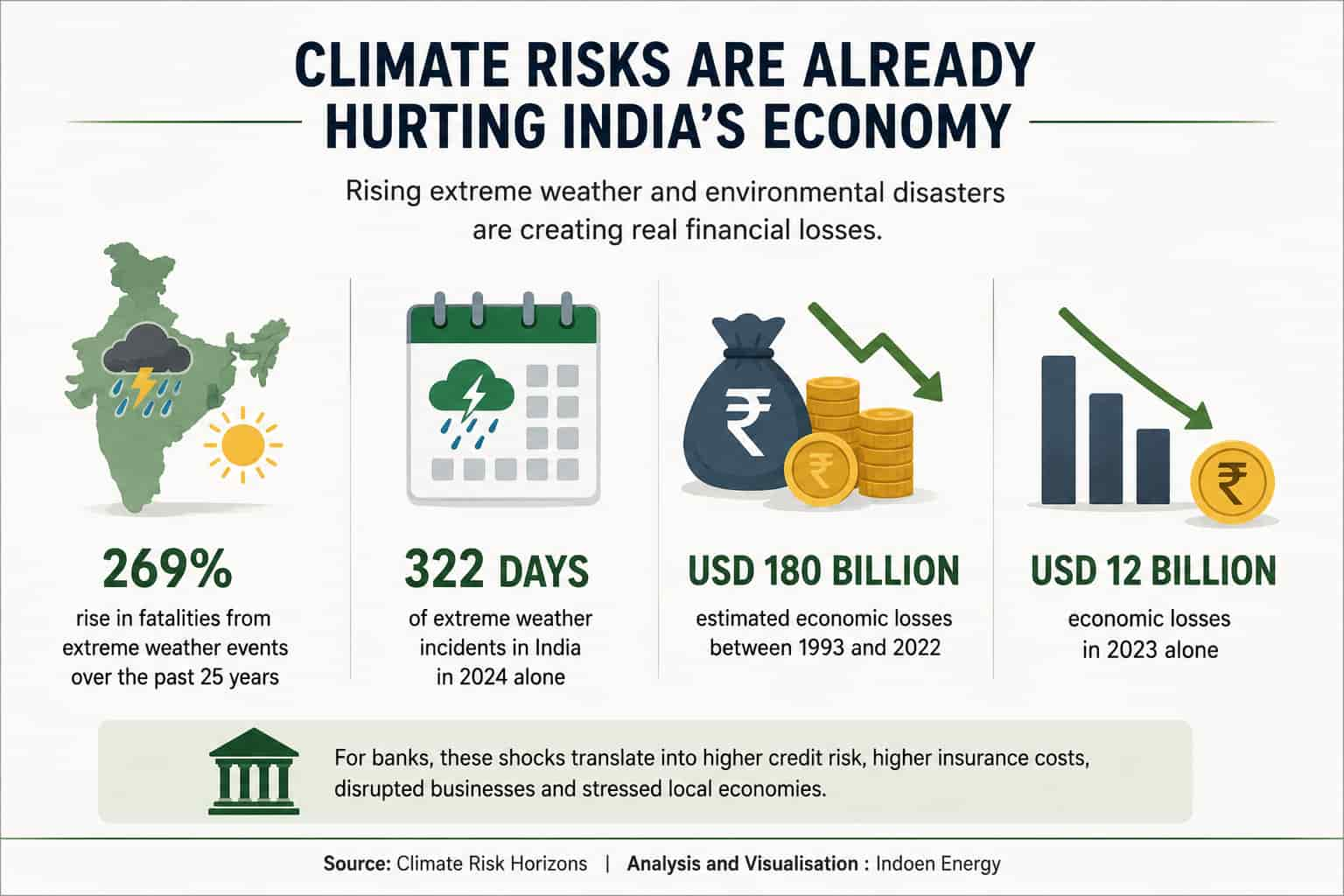

India’s climate crisis is no longer theoretical.

Fatalities linked to extreme weather events have reportedly surged by nearly 269% over the past 25 years, while 2024 alone witnessed extreme weather incidents on 322 days. Economic losses between 1993 and 2022 touched an estimated USD 180 billion, with another USD 12 billion lost in 2023 alone.

For banks, these are not merely environmental statistics.

Crop failures affect agricultural loans. Floods disrupt industrial operations and infrastructure assets. Heatwaves damage labour productivity and power systems. Insurance costs rise. Mortgage risks escalate in vulnerable regions. Entire local economies become unstable.

The financial sector sits at the centre of these cascading risks.

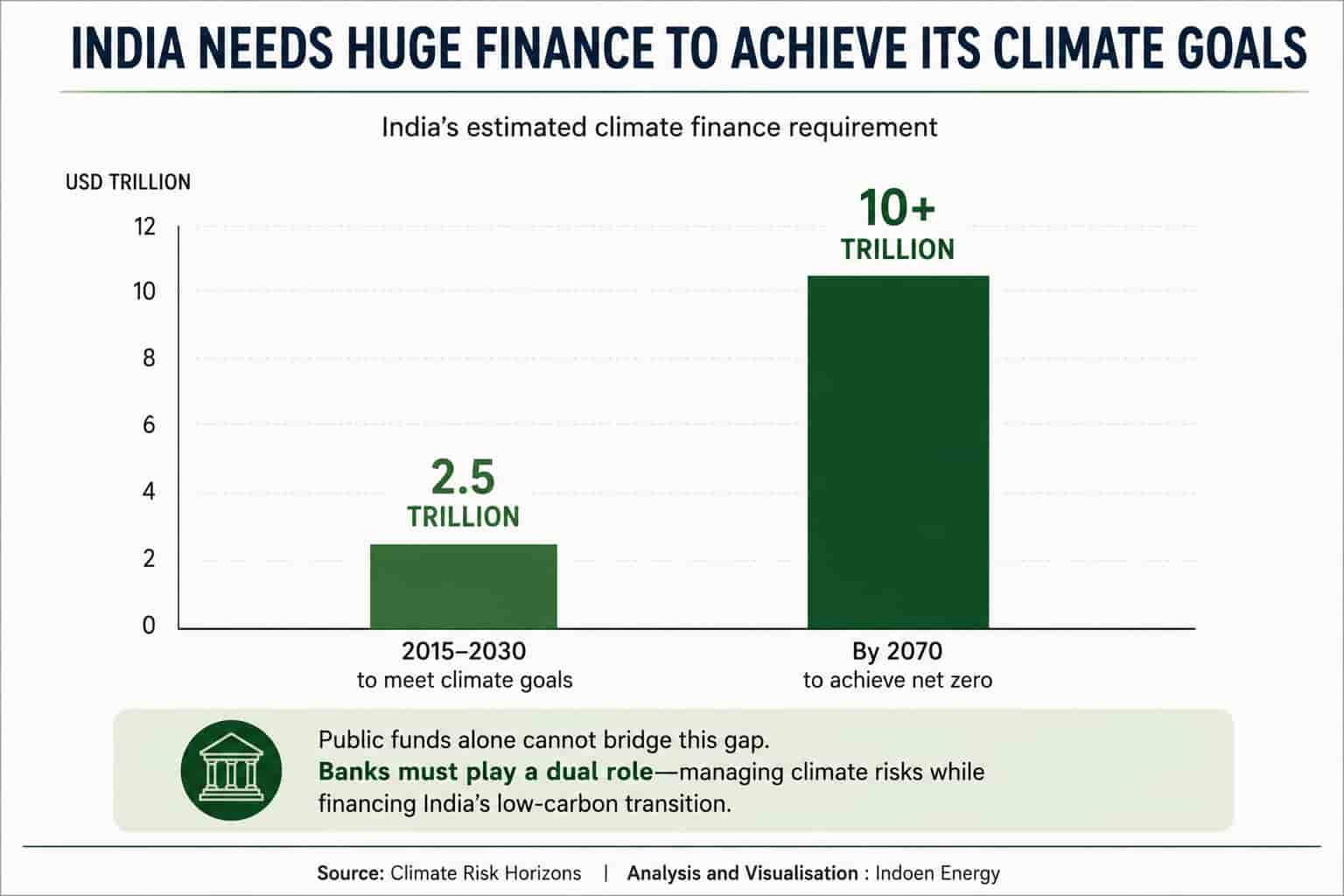

At the same time, India’s transition ambitions require enormous capital mobilisation.

The country estimates that it needs roughly US$2.5 trillion between 2015 and 2030 to meet climate goals and more than USD 10 trillion to achieve net zero by 2070. Public funding alone cannot bridge this gap.

Banks are therefore expected to play a dual role: protecting themselves from climate-linked financial shocks while also financing India’s low-carbon transition.

That balancing act is proving difficult.

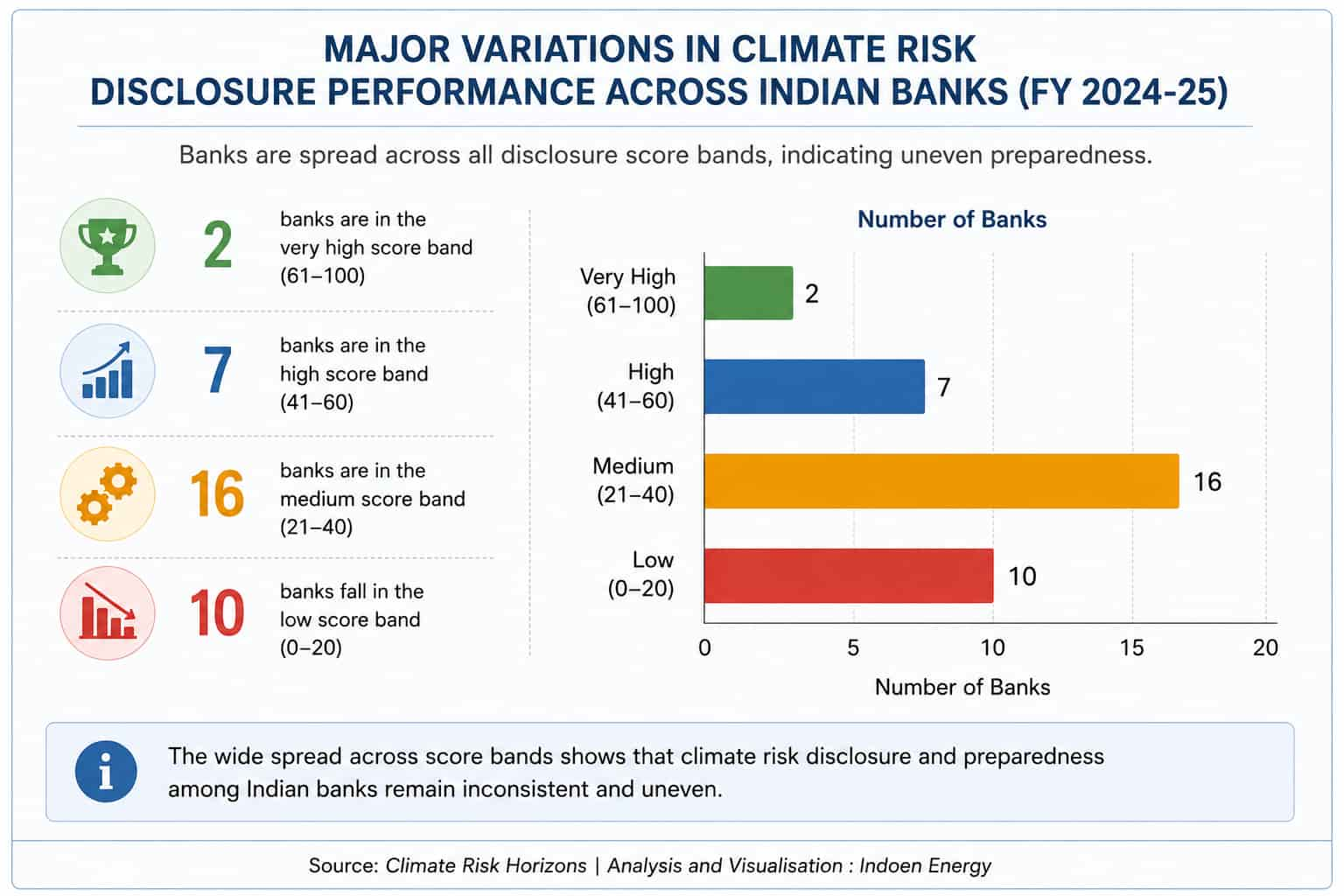

Progress exists — but mostly on paper

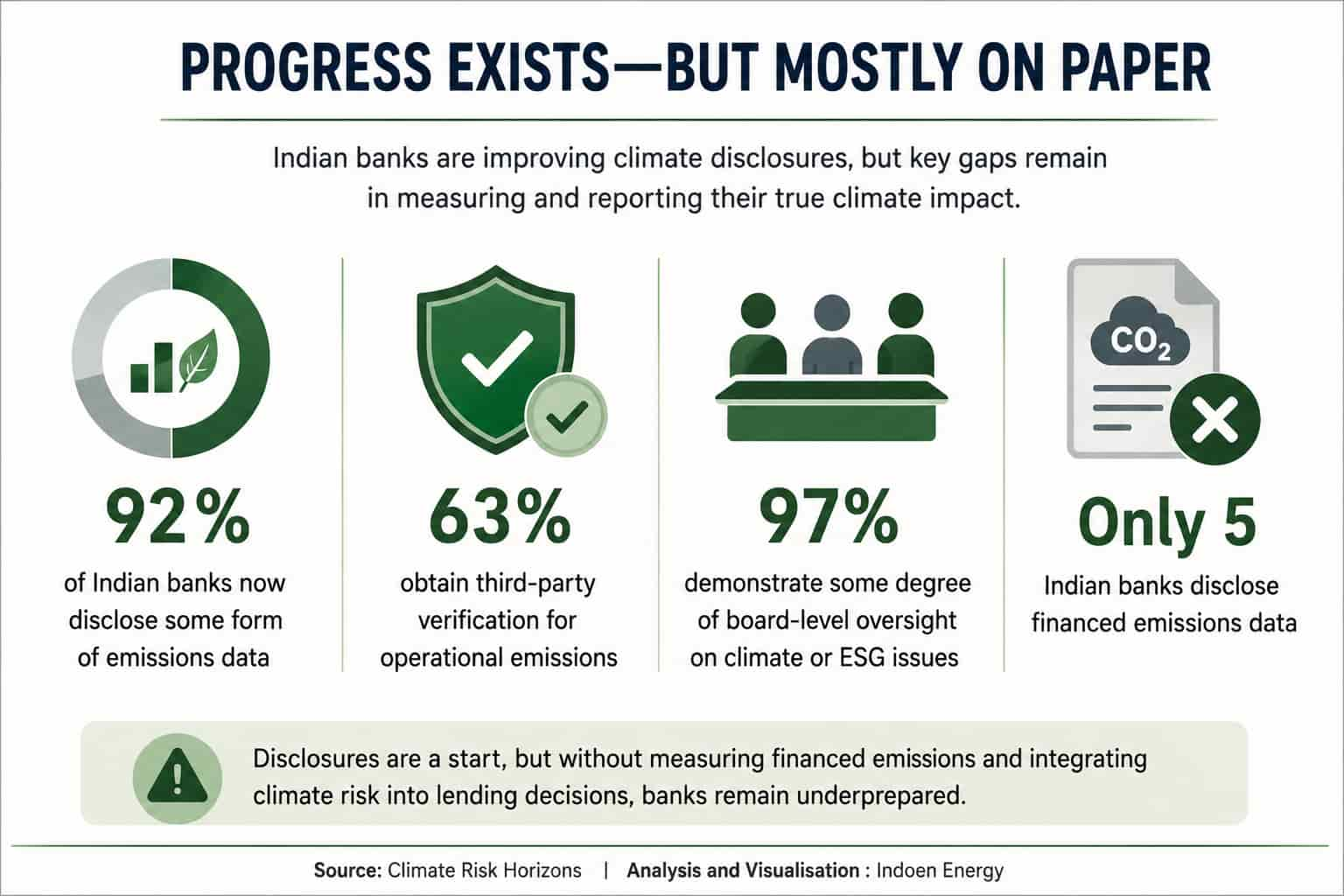

The encouraging part is that Indian banks are no longer ignoring climate disclosures.

According to Climate Risk Horizon report, 92% of Indian banks now disclose some form of emissions data, 63% obtain third-party verification for operational emissions, and 97% demonstrate some degree of board-level oversight on climate or ESG issues.

This marks substantial progress compared to 2022, when fewer than half of banks disclosed emissions information.

But disclosures alone do not necessarily translate into preparedness.

Many banks continue to focus primarily on operational emissions — the emissions generated from offices, branches and operations — while neglecting financed emissions, which arise from the activities they lend money to. These financed emissions represent the overwhelming majority of a bank’s climate footprint.

Only five Indian banks currently disclose financed emissions data. Even fewer have obtained external verification. The International Financial Reporting Standards Foundation (IFRS) has already moved toward tighter financed-emissions disclosure expectations globally, especially for banks and asset managers.

That gap matters enormously because a bank financing coal plants, oil infrastructure or high-emission industries may face substantial transition risks in the coming decades, regardless of how energy-efficient its own buildings become.

The divide between ‘disclosure readiness’ and ‘risk readiness’ is becoming increasingly visible.

Coal remains the elephant in the room

Perhaps the most striking weakness in India’s banking sector is the absence of serious coal phase-out policies.

Despite global momentum toward energy transition, only Federal Bank and RBL Bank have explicit coal phase-out commitments. Union Bank of India has made a limited pledge toward gradually reducing thermal coal exposure, though without a time-bound roadmap.

This stands in sharp contrast to international banking trends.

Major global lenders are increasingly tightening restrictions on coal financing under pressure from investors, regulators and climate litigation risks. Several European and North American banks have committed to ending direct financing for new coal projects.

Indian banks, however, remain deeply exposed to fossil-linked sectors.

Part of this hesitation reflects India’s developmental reality. Coal still underpins a large share of the country’s electricity generation and industrial activity. Policymakers remain cautious about imposing abrupt financial restrictions that could disrupt energy security or industrial growth.

But that caution also creates long-term financial vulnerability.

As renewable energy costs continue falling and global carbon regulations tighten, coal-linked assets could rapidly lose value. Banks heavily exposed to such sectors may eventually face rising defaults, asset impairment and capital adequacy pressures

An executive at a Mumbai-based sustainable finance advisory firm noted privately that many Indian lenders “still see coal as a sovereign comfort sector rather than a transition liability.”

That perception may not survive the next decade.

Stress testing remains shallow

One of the clearest signs that climate risk integration remains immature is the state of climate stress testing.

Fourteen Indian banks say they have initiated climate scenario analysis or stress-testing exercises. Yet none has publicly disclosed how these scenarios could impact capital buffers, asset quality or profitability.

In many cases, banks simply acknowledge that climate stress testing is ‘underway’ without providing meaningful methodological transparency.

Globally, however, regulators are increasingly demanding exactly such disclosures.

The Network for Greening the Financial System has developed increasingly sophisticated climate scenarios covering both physical and transition risks. The Financial Stability Board has released frameworks to help regulators identify climate-linked vulnerabilities across credit, liquidity and market channels.

Meanwhile, the Bank for International Settlements has begun exploring ways to integrate physical climate risk into conventional credit-risk models.

Indian banks may soon face pressure to align with these evolving global norms.

The net-zero problem

Net-zero commitments among Indian banks remain surprisingly weak.

Only six out of 35 banks assessed have announced net-zero targets, and merely two — State Bank of India and Punjab National Bank — include Scope 3 financed emissions within those goals.

Most others restrict targets to operational emissions alone.

That creates a paradox where a bank may claim ‘carbon neutrality’ while continuing to finance highly emission-intensive sectors without any decarbonisation pathway.

Globally, investor scrutiny around such inconsistencies is rising.

Financial institutions increasingly face accusations of greenwashing when climate commitments exclude lending portfolios.

International investors, sovereign funds and ESG-focused asset managers are becoming more demanding about financed emissions disclosure and transition alignment.

India’s banking sector could face similar scrutiny as cross-border capital flows become increasingly climate-sensitive.

The adaptation blind spot

One of the more important insights emerging from climate reports is the limited attention being paid to climate adaptation.

Much of the climate finance debate globally still revolves around emissions reduction. But India’s immediate financial risks increasingly stem from physical climate impacts already underway.

Floods damaging infrastructure loans. Droughts affecting rural credit systems. Heat stress disrupting industrial productivity. Coastal erosion threatening real estate values.

Banks may soon discover that adaptation finance is not simply a developmental issue but a core financial stability issue.

That shift could open major investment opportunities.

Climate-resilient infrastructure, water management systems, disaster-resilient housing, cooling technologies and resilient agricultural systems are likely to become major financing themes over the next decade.

Several industry analysts believe Indian banks that move early into adaptation-linked financing could eventually gain competitive advantages as climate-resilient sectors attract policy support and global capital.

A global financial transition is underway

What makes the current moment especially significant is that climate finance is rapidly becoming embedded into mainstream financial architecture worldwide.

The IFRS Foundation has revised climate disclosure standards. UNEP FI is helping banks integrate 1.5°C pathways into portfolio planning. Central banks are building climate-risk supervision into prudential regulation.

Even conservative financial institutions increasingly acknowledge that climate change is no longer a niche ESG concern.

It is becoming a balance-sheet issue.

India cannot remain insulated from that transformation.

Foreign capital increasingly flows toward markets perceived as transition-ready. Export competitiveness is becoming tied to carbon intensity. Carbon border taxes are emerging in major economies. Climate disclosure standards are converging internationally.

Banks that fail to adapt may eventually face both financial and reputational disadvantages.

Compliance will not be enough

The deeper issue is philosophical.

Many Indian banks still appear to treat climate risk as a reporting exercise rather than a structural economic shift capable of reshaping entire sectors.

That mindset may become increasingly dangerous.

Climate transition is likely to alter industrial competitiveness, asset valuations, lending priorities and sovereign risk assessments over the coming decades. Financial institutions that merely comply with disclosure rules without fundamentally rethinking portfolio strategy may find themselves exposed to risks they neither measured nor anticipated.

India’s banking system still has time to adapt. But the window for gradualism is narrowing.

The transition from ‘climate disclosure’ to ‘climate accountability’ has already begun globally. Once regulators start demanding capital allocation changes, financed-emissions transparency and measurable transition pathways, the sector may be forced into much faster adjustments.

For now, Indian banks appear to be taking small steps toward a very large problem.

The concern is whether those steps are arriving quickly enough.