India’s clean-energy transition has largely been shaped by the rapid expansion of solar power, wind energy, battery storage and, more recently, green hydrogen. Yet a quieter energy source buried beneath the country’s surface is beginning to re-enter policy and industrial discussions with unusually large numbers attached to it.

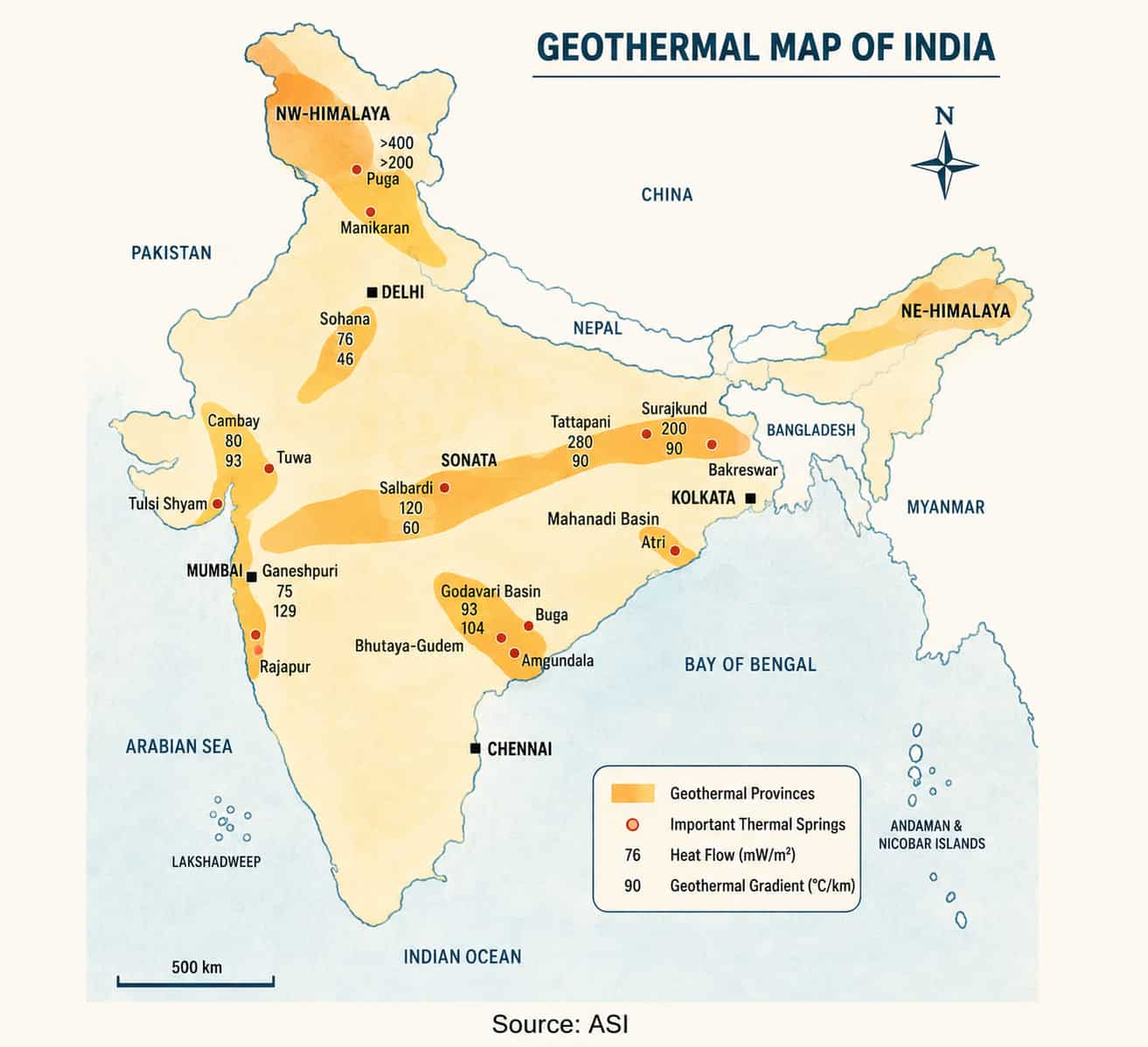

A recent report highlighted that India could theoretically unlock nearly 11,000 GW of geothermal heating potential, over 1,500 GW of cooling potential, and around 450 GW of electricity generation capacity. While much of the public attention has focused on the electricity figure, the more consequential story may lie elsewhere: industrial heat and cooling.

At a time when India is grappling with rising electricity demand, industrial decarbonisation pressures, climate-linked heat stress and concerns over round-the-clock clean power, geothermal energy is increasingly being viewed not merely as another renewable source but as a potentially strategic infrastructure layer in the country’s evolving energy system.

That possibility is gaining relevance precisely because India’s transition is entering a more difficult phase.

Beyond electricity: The industrial heat challenge

Much of India’s renewable-energy success has come from electricity generation. Solar tariffs collapsed over the past decade, renewable installations accelerated, and battery storage investments have started scaling rapidly.

However, industrial heat — required for sectors such as steel, chemicals, textiles, cement, food processing and pharmaceuticals — remains one of the hardest areas to decarbonise globally.

This is where geothermal could acquire strategic significance.

Unlike solar and wind, geothermal systems can provide continuous thermal energy without depending on weather conditions. That makes them particularly relevant for industrial clusters that require stable heat and cooling systems throughout the day.

The new geothermal estimates suggest India’s underground resources may hold significantly larger thermal value than previously recognised.

Globally, industrial heat accounts for nearly one-fifth of total energy-related carbon emissions, according to the International Energy Agency. Yet it remains one of the least discussed components of the clean-energy transition.

For India, the timing is notable.

The country is simultaneously pursuing manufacturing expansion, data-centre growth, semiconductor ambitions and export-oriented industrialisation. Each of these trends could sharply increase energy intensity and cooling requirements over the coming decade.

The rise of “24x7 clean energy”

One of the biggest structural challenges facing India’s renewable transition is reliability.

Solar generation peaks during daytime. Wind output fluctuates seasonally. Battery storage is improving rapidly but remains capital-intensive at scale. This has led policymakers and industry planners to increasingly focus on “24x7 clean power” systems that combine multiple technologies.

Geothermal fits naturally into that conversation because it provides firm, non-intermittent energy.

That characteristic is becoming strategically valuable as India’s electricity demand surges. The country’s peak power demand crossed 250 GW in 2024 and could exceed 400 GW by 2030 under several projections.

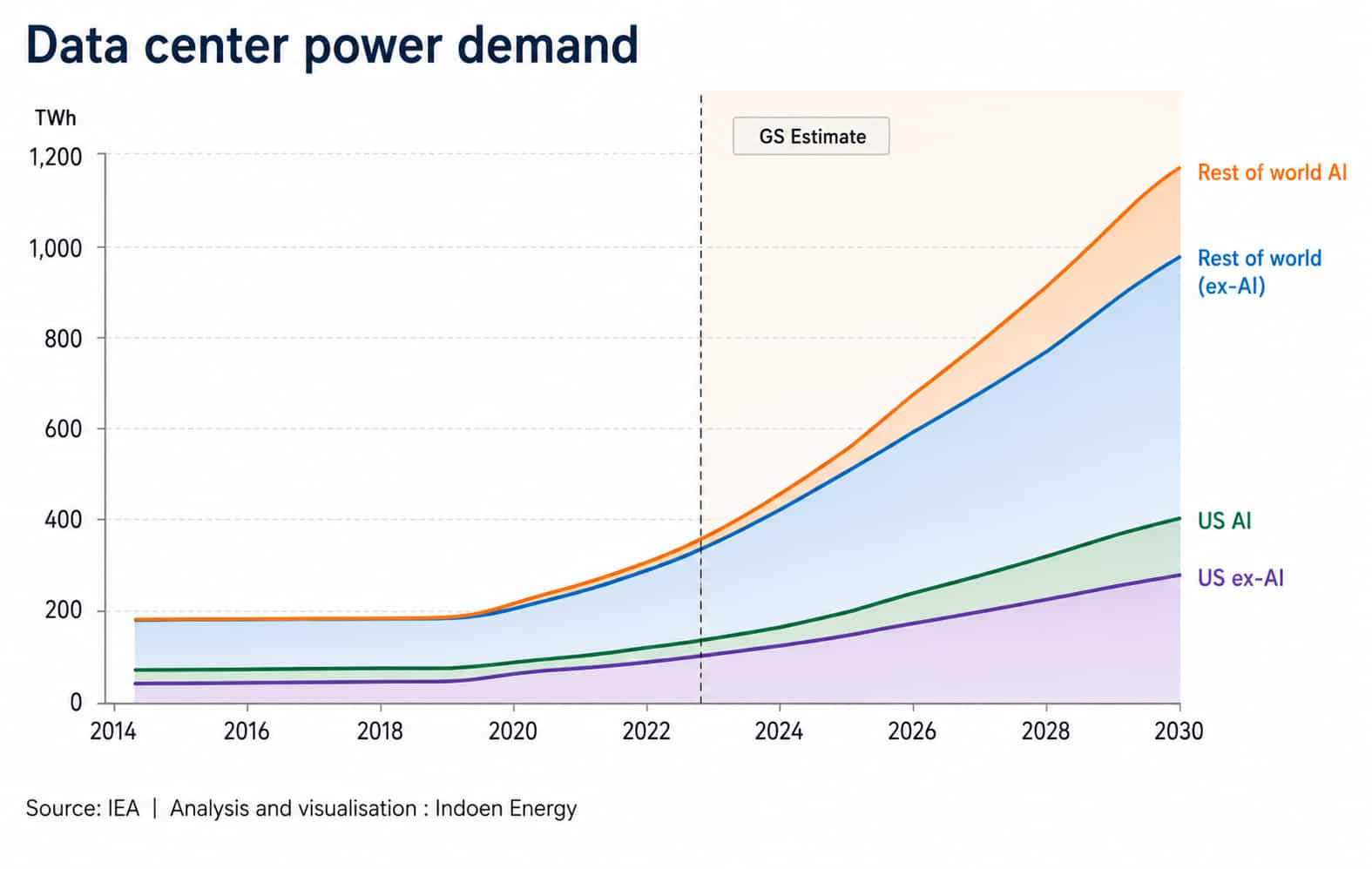

The rise of artificial intelligence infrastructure may intensify those pressures further.

Globally, major technology companies are increasingly exploring geothermal energy for data centres because of its stable power profile and cooling applications. In the United States, companies including Google and Microsoft-backed ventures have invested in advanced geothermal systems as AI-linked electricity demand rises sharply.

India’s own data-centre market is projected to attract billions of dollars in investments over the next several years, particularly across Mumbai, Chennai, Hyderabad and Noida. Cooling demand from these facilities is expected to become a major electricity challenge.

That creates an unusual overlap between geothermal cooling potential and India’s digital infrastructure ambitions.

A hidden energy-security story

Geothermal also intersects with a broader geopolitical concern: energy security.

India remains heavily dependent on imported fossil fuels, particularly crude oil, LNG and coking coal. Volatility in global fuel markets — intensified by conflicts in Europe and West Asia — has repeatedly exposed the vulnerability of import-dependent economies.

Unlike imported fuels, geothermal energy is domestic, weather-independent and largely immune to maritime disruptions or global commodity cycles.

That could make geothermal particularly attractive for remote industrial zones, Himalayan regions and strategically sensitive border areas.

Ladakh has long been viewed as India’s most visible geothermal prospect, especially around Puga Valley. However, newer assessments suggest geothermal applications may extend beyond Himalayan pilot projects into broader industrial and urban use cases.

One emerging possibility is district cooling systems powered partly by geothermal resources in dense urban clusters.

As India’s cooling demand accelerates due to rising temperatures and urbanisation, cooling itself is becoming a major energy-policy issue. The India Cooling Action Plan estimates that cooling demand could rise nearly eightfold by 2037-38.

That means geothermal’s cooling potential may eventually prove as important as its electricity-generation prospects.

Why geothermal is returning now

India has explored geothermal possibilities for decades, but commercial progress remained negligible because of high drilling costs, limited policy support and technological constraints.

What may be changing now is the global economics of drilling.

Advanced drilling techniques originally developed for the oil-and-gas industry are reducing geothermal exploration costs internationally. Enhanced geothermal systems, deeper drilling capabilities and improved reservoir mapping technologies are reviving investor interest globally.

According to the International Energy Agency, global geothermal investment momentum is strengthening as countries search for firm low-carbon energy sources that can complement renewables.

This trend is particularly visible in the United States, Indonesia, Kenya and parts of Europe.

Indonesia, for instance, has aggressively expanded geothermal generation to reduce coal dependence and improve grid stability. Kenya now sources a major portion of its electricity from geothermal power, demonstrating how the resource can reshape national energy systems under favourable geological conditions.

India’s geology differs substantially, and direct comparisons may be misleading. Yet the global shift itself matters because it could attract technology partnerships, foreign investment and new policy attention.

The financing problem remains formidable

Despite the optimism, geothermal remains commercially uncertain in India.

Exploration risk is one of the biggest barriers. Unlike solar or wind projects, geothermal drilling can require significant upfront investment without guaranteed returns.

Industry executives note that financing institutions often remain reluctant because geothermal projects involve long gestation periods, geological uncertainty and limited domestic operational experience.

That creates a policy contradiction.

India wants deeper industrial decarbonisation and round-the-clock clean energy, but the financing ecosystem still heavily favours established technologies such as solar and wind.

Without exploration-risk guarantees, concessional finance or public-private partnerships, geothermal deployment may remain confined to pilot projects.

Another challenge involves infrastructure integration.

Many geothermal-rich regions are located away from major industrial corridors, requiring transmission networks, thermal-distribution systems or localised industrial ecosystems to become commercially viable.

The larger transition story

The geothermal discussion ultimately reflects a broader shift in India’s energy transition.

The first phase of the transition focused on adding renewable capacity quickly. The next phase is increasingly about system reliability, industrial competitiveness, energy security and infrastructure resilience.

That transition is forcing policymakers to look beyond headline renewable numbers toward technologies capable of supporting stable industrial growth.

The surprising aspect is that geothermal may become more important because of what solar and wind achieved — not despite them.

As renewable penetration rises, the value of firm clean power increases sharply.

That could eventually transform geothermal from a niche resource into part of a wider hybrid energy architecture involving storage, renewable generation, industrial heating systems and district cooling networks.

For now, India’s geothermal ambitions remain largely theoretical.

But the conversation itself signals something deeper: the country’s clean-energy transition is beginning to move from an era of capacity expansion into a far more complex debate about how to build a continuously powered, industrial-scale, low-carbon economy.

And in that emerging debate, underground heat may no longer remain invisible.