India’s green hydrogen ambitions are rapidly evolving from a government-backed clean-energy vision into a potentially massive industrial and export opportunity worth nearly US$7.4 billion, as energy companies, infrastructure developers and financial markets reposition themselves around what could become the country’s next major energy growth story.

The sector’s accelerating momentum reflects a broader global shift in which hydrogen is increasingly viewed not merely as a climate solution, but as a strategic industrial fuel capable of reshaping manufacturing, shipping, fertilisers, steel production and international energy trade.

Recent developments — including export-oriented agreements, production-linked incentives, electrolyser manufacturing investments and rising investor interest in hydrogen-linked companies — suggest that India is now entering a more commercially serious phase of the hydrogen transition.

Industry estimates cited across recent market reports indicate that India’s emerging hydrogen ecosystem could unlock opportunities worth around ₹70,000 crore, or roughly $7.4 billion at current exchange rates.

The figure is increasingly attracting the attention of investors who believe hydrogen may eventually follow a trajectory similar to solar energy — though potentially with deeper industrial implications.

India’s hydrogen push is becoming export-driven

One of the most important shifts underway is the growing emphasis on exports.

A recent memorandum of understanding involving GH2 Solar and international partners highlighted how Indian hydrogen projects are increasingly being designed around overseas demand, particularly from Europe and East Asia, where industries are under pressure to decarbonise heavy manufacturing and shipping operations.

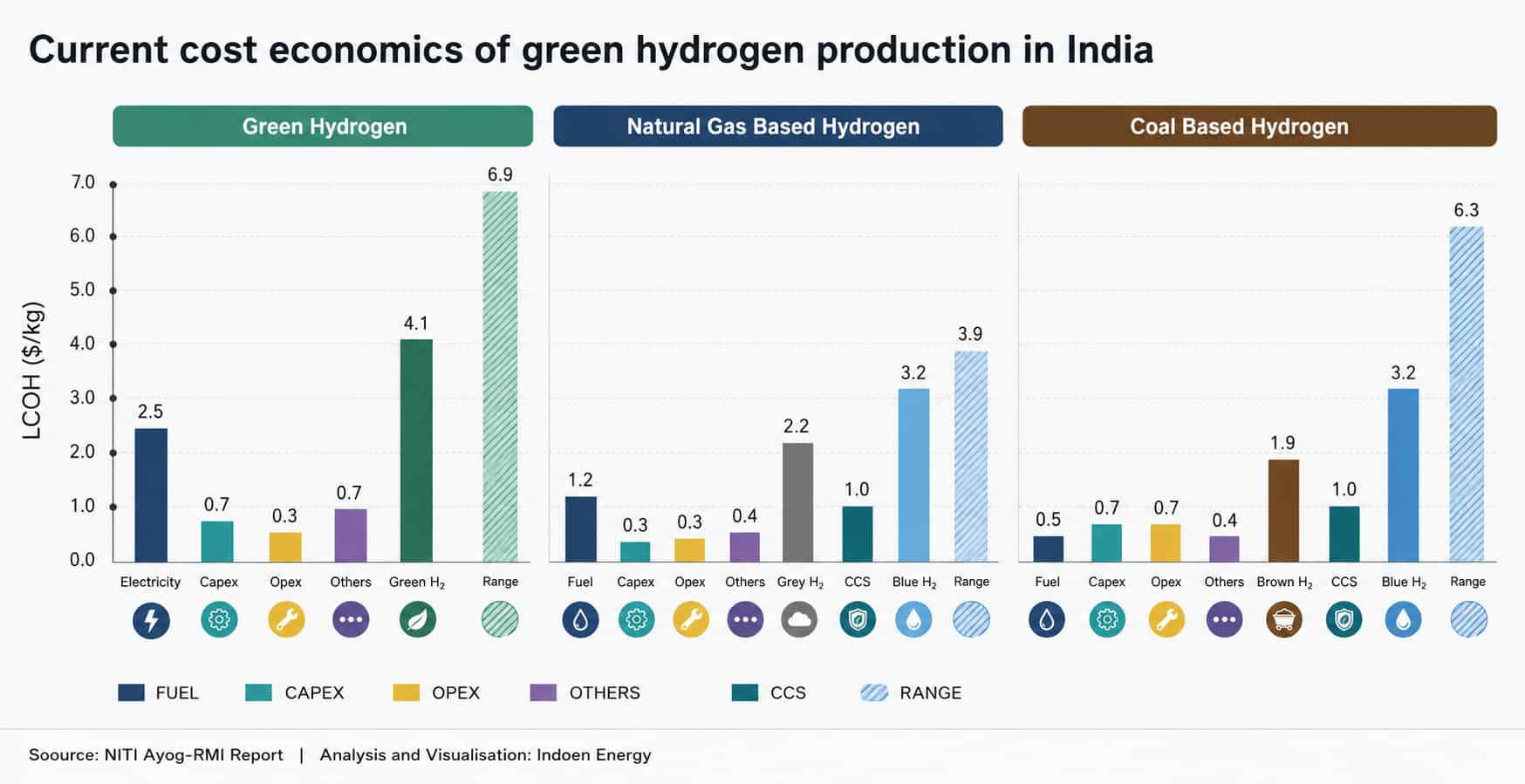

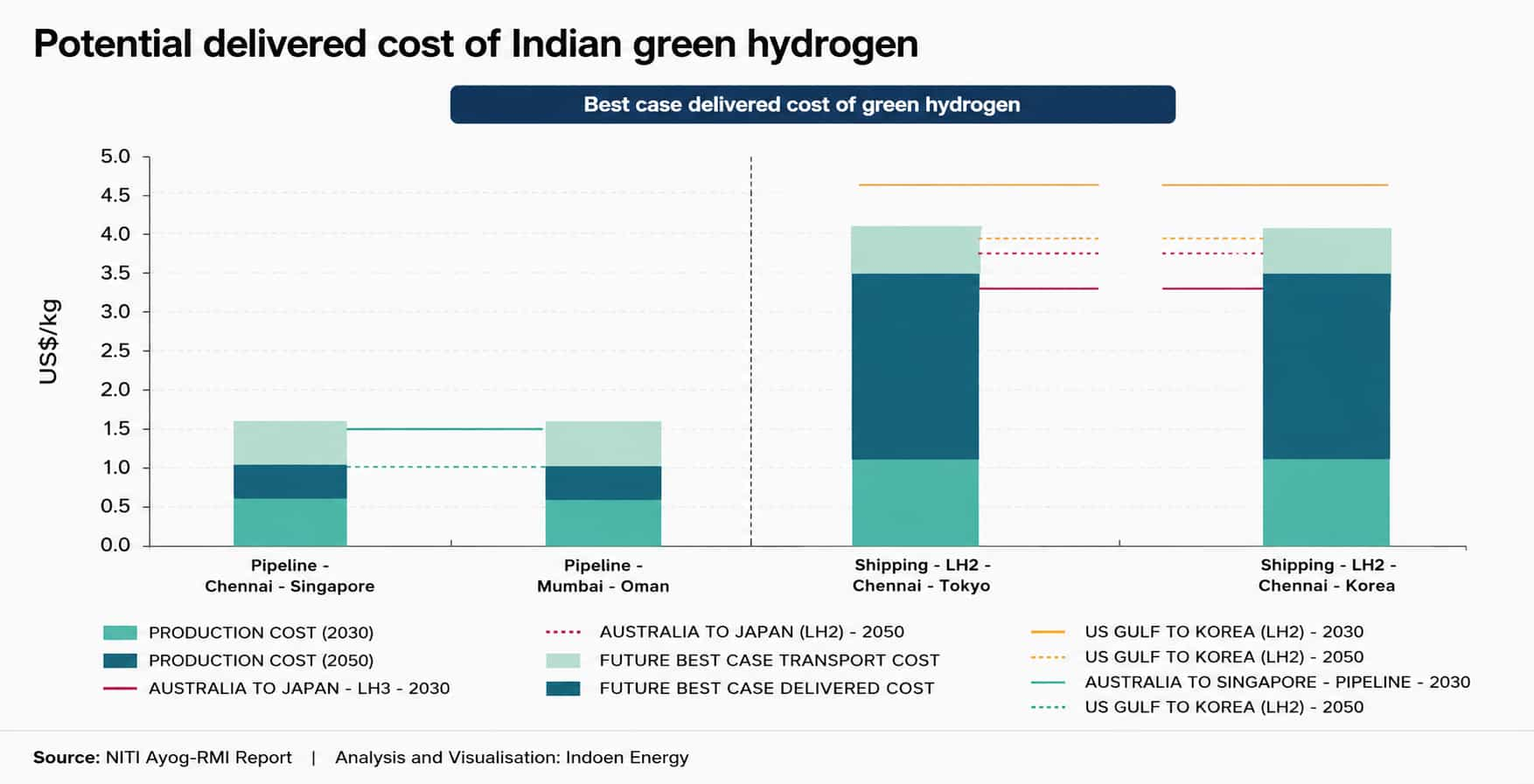

This export focus matters because the economics of green hydrogen remain challenging within domestic markets alone. Producing hydrogen using renewable electricity is still considerably more expensive than conventional fossil-fuel-based hydrogen.

Current estimates suggest India’s green hydrogen production costs range between roughly ₹397 and ₹560 per kilogram ($4.6–$6.7/kg) depending on renewable electricity tariffs, electrolyser efficiency and financing costs.

However, India possesses one major structural advantage that many competing economies lack: some of the world’s cheapest solar and renewable power.

That cost advantage is becoming strategically important as Europe, Japan and South Korea increasingly seek long-term imports of green ammonia and hydrogen derivatives to meet industrial decarbonisation targets.

Several sector analysts now believe India could eventually emerge as a major supplier of green industrial fuels rather than simply a domestic consumer market.

The policy ecosystem is expanding far beyond headline incentives

India’s hydrogen ambitions are also being strengthened by a rapidly expanding industrial policy framework.

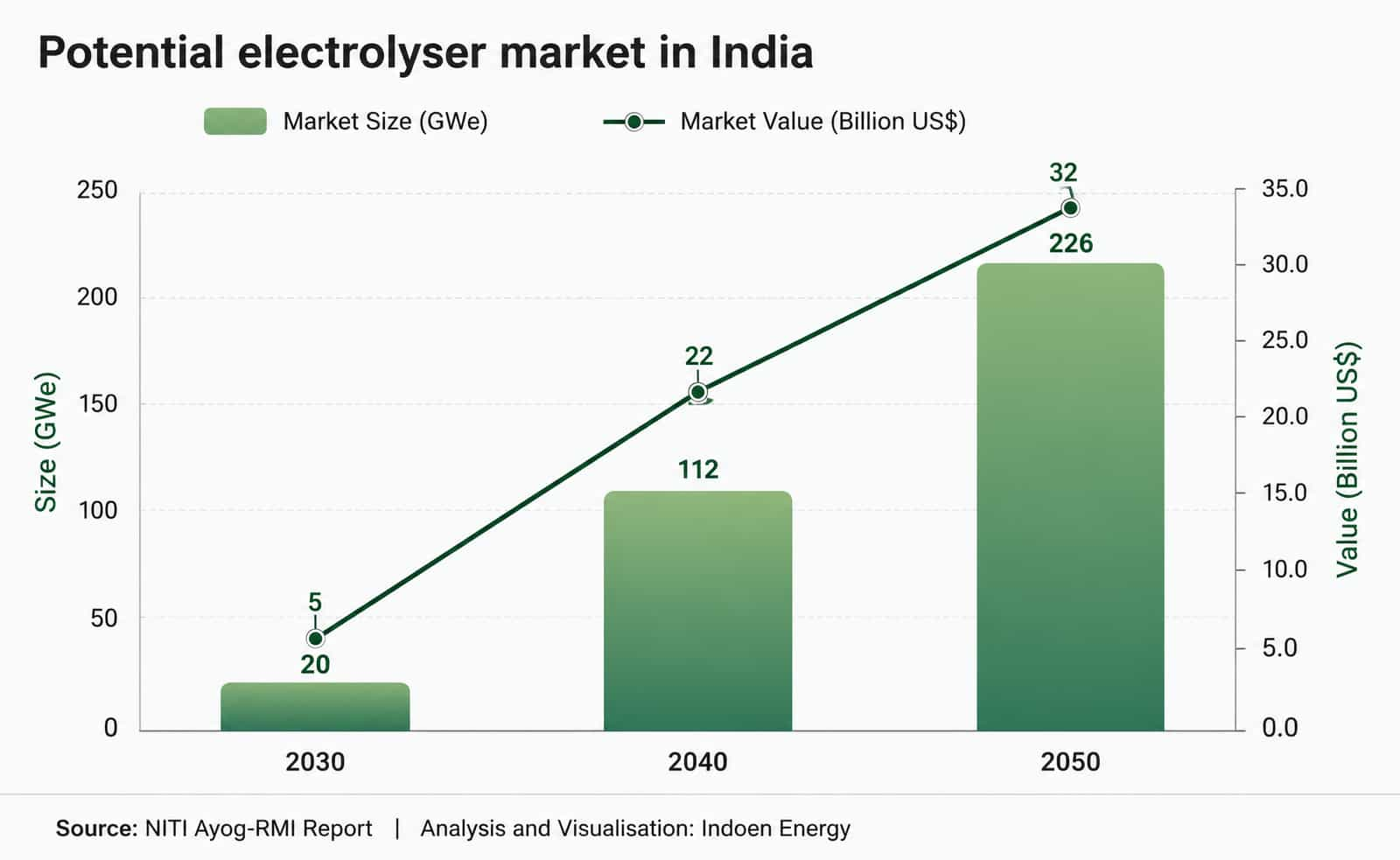

Under the National Green Hydrogen Mission, the government has introduced incentive structures for electrolyser manufacturing, hydrogen production, pilot projects and associated infrastructure development.

Government data released this year showed that companies had already secured allocations for thousands of megawatts of electrolyser manufacturing capacity under support schemes worth ₹4,440 crore (US$464 million).

Another set of approved projects involves annual green hydrogen production capacity exceeding 8,60,000 tonnes.

Yet one of the lesser-known aspects of India’s hydrogen strategy is the scale of indirect support mechanisms emerging around the sector.

A recent policy analysis suggested that combined central and state-level subsidies, transmission waivers, tax incentives and infrastructure support mechanisms could collectively amount to nearly ₹5 lakh crore (US$52.3 billion) over time.

That effectively transforms hydrogen into one of India’s largest emerging industrial-policy experiments outside semiconductors and electronics manufacturing.

Hydrogen could reshape India’s industrial geography

One of the most striking long-term implications is how hydrogen is beginning to influence India’s future industrial map.

Renewable-rich states such as Gujarat, Rajasthan, Tamil Nadu, Andhra Pradesh and Odisha are increasingly positioning themselves as future hydrogen hubs because they combine solar or wind resources with industrial corridors and port access.

This is creating a new kind of industrial clustering model where renewable power, ports, ammonia export terminals, heavy manufacturing and hydrogen production facilities may eventually operate as integrated ecosystems.

A major ‘wow factor’ emerging from industry studies is the enormous scale of supporting electrical infrastructure required.

Some estimates suggest electrical systems can account for 30-50% of the total cost of large electrolyser projects. For a single 100 MW electrolyser facility, electrical infrastructure costs alone could exceed ₹1,000 crore (US$104.6 million).

That means hydrogen may generate substantial secondary demand for grid infrastructure companies, power equipment manufacturers, industrial automation firms and transmission-system suppliers.

Financial markets are beginning to reposition early

Indian financial markets are also beginning to treat hydrogen as a long-term structural investment theme rather than a speculative clean-energy niche.

Recent market commentary has increasingly focused on hydrogen-linked firms connected to industrial gases, electrolysers, renewable power infrastructure and ammonia exports.

Unlike the earlier renewable-energy boom centred mainly on electricity generation, hydrogen potentially creates a globally tradable industrial commodity market.

Some industry executives increasingly compare hydrogen’s future significance to the rise of LNG markets decades ago — particularly for countries aiming to dominate future low-carbon industrial supply chains.

Studies suggest that successful domestic hydrogen adoption could eventually help India reduce fossil-fuel imports by billions of dollars annually.

The economics still remain difficult

Despite the optimism, the sector still faces major implementation risks.

Green hydrogen projects remain heavily dependent on low-cost financing, policy support and renewable electricity availability.

Many announced projects globally have struggled to reach commercial viability because hydrogen production remains capital-intensive and demand visibility is still uncertain.

There are also growing concerns regarding water availability in renewable-rich but arid regions, land acquisition pressures and potential competition from lower-cost hydrogen exporters in the Middle East and Latin America.

Another challenge is timing.

Several analysts believe the global hydrogen sector may initially experience a period of overinvestment before demand scales sufficiently to absorb planned production capacity.

That creates the possibility of pricing pressure, delayed returns and project restructuring during the sector’s early years.

India is entering a geopolitical fuel race

Perhaps the most important long-term implication is geopolitical.

Hydrogen is increasingly becoming part of a wider global competition over future industrial leadership, green manufacturing and strategic energy trade routes.

Countries capable of producing low-cost green hydrogen could eventually gain influence over sectors ranging from steel and fertilisers to shipping fuels and carbon-conscious manufacturing supply chains.

India’s vast renewable-energy expansion, relatively low solar costs and growing industrial base position it uniquely within that race.

What makes the current phase especially significant is that hydrogen is no longer being discussed merely as an environmental obligation. It is increasingly being framed as a strategic economic opportunity capable of reshaping industrial investment, export competitiveness and long-term energy security.

The sector still faces substantial economic and technological uncertainties.

But after years of remaining largely conceptual, India’s hydrogen economy is finally beginning to acquire industrial scale, financial momentum and geopolitical relevance simultaneously.