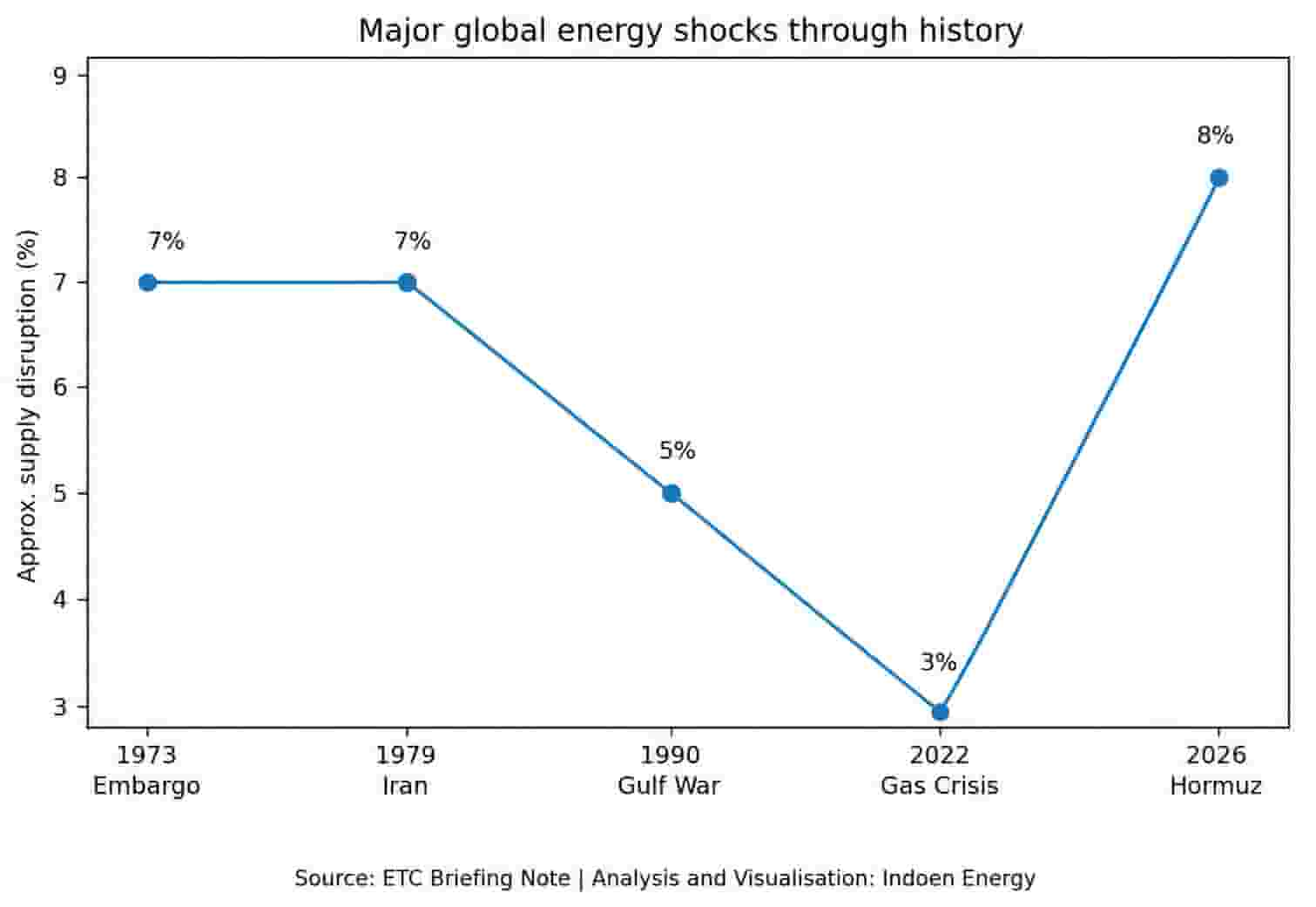

For decades, the Strait of Hormuz has represented one of the world’s greatest geopolitical vulnerabilities. Yet, it seems, even seasoned energy strategists underestimated how profoundly the 2026 Hormuz crisis would shake the global economy.

What began as a regional military confrontation involving Iran, Israel and the United States rapidly evolved into something much larger — a full-spectrum stress test of the fossil fuel age itself.

The crisis did not simply send oil prices soaring. It exposed a deeper structural weakness embedded within the global economic system: modern civilisation still depends heavily on geographically concentrated fossil fuel flows moving through narrow maritime chokepoints vulnerable to war, sabotage, sanctions and political coercion.

Within weeks, the effects spread across continents. Oil prices surged above US$100 per barrel. Asian LNG prices doubled. Fertiliser costs spiked. European electricity markets convulsed again. Airlines struggled with jet fuel shortages. Food inflation fears resurfaced.

In parts of South Asia, restaurants reverted to wood-fired cooking as LPG shortages intensified. According to reports Europe’s jet fuel imports from the Middle East collapsed sharply after the disruption, forcing buyers to seek alternative supply chains from the United States and Africa.

But amid the turmoil, another trend accelerated quietly in the background. Governments, investors and industries increasingly began treating clean energy not merely as a climate obligation but as a strategic defence against future geopolitical shocks.

That shift may ultimately become the defining consequence of the Hormuz crisis.

The chokepoint that still controls the global economy

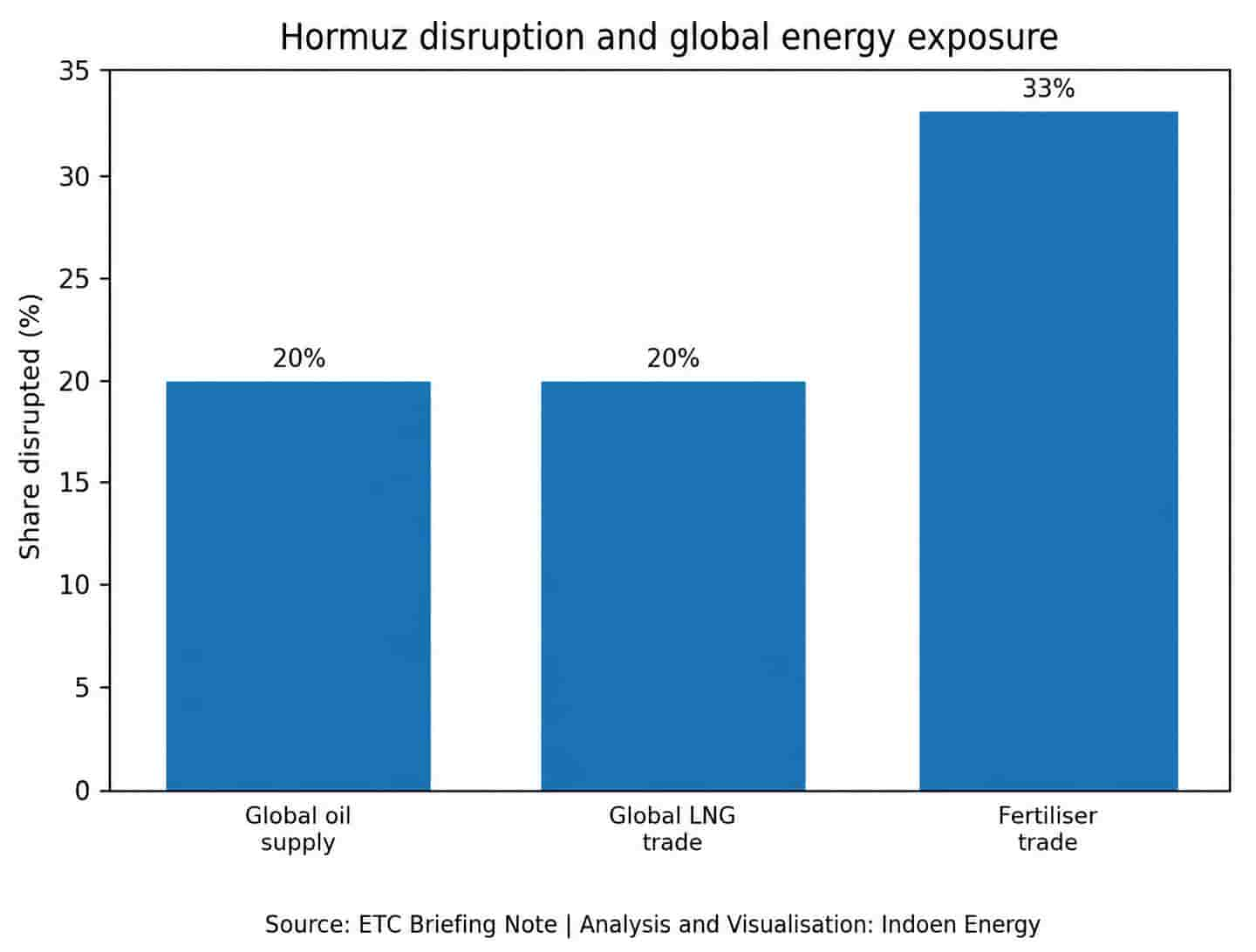

The Strait of Hormuz handles roughly one-fifth of global oil and LNG trade. No other maritime corridor exerts such enormous influence over the functioning of the world economy. Nearly 18 million barrels of crude oil and petroleum products move daily through the narrow passage between Iran and Oman.

Yet the disruption extended far beyond oil and gas.

The Gulf region is deeply integrated into fertiliser, petrochemical and industrial metals supply chains. Roughly one-third of globally traded fertiliser inputs transit through Hormuz. Sulphur exports essential for battery metals processing and copper extraction were also disrupted, exposing vulnerabilities even within parts of the clean energy supply chain itself.

The crisis therefore rapidly spread into agriculture, manufacturing and food systems.

In India, fertiliser prices surged. LPG shortages affected households and restaurants. In Sri Lanka, fuel rationing fears returned. Across Africa, higher diesel prices threatened transport affordability and food logistics. Europe faced another wave of gas-driven industrial anxiety reminiscent of the Ukraine crisis. The International Monetary Fund warned that disruptions to Gulf oil, gas and fertiliser flows could significantly weaken global growth while worsening inflation and living costs worldwide.

The world was reminded once again that fossil fuel disruptions are never merely energy stories. They become inflation stories, political stories, industrial stories and, eventually, social stability stories.

Why Asia became the frontline of the crisis

Although the shock reverberated globally, Asia absorbed the most severe damage.

More than 80% of Hormuz-linked oil and LNG flows are directed towards Asian markets. Economies such as India, China, Japan, South Korea, Pakistan and Bangladesh remain deeply dependent on Gulf hydrocarbons for electricity, transport fuels, petrochemicals and cooking gas.

That dependence translated into immediate vulnerability.

In poorer Asian economies, energy inflation rapidly spilled into everyday life because households spend a far greater share of income on fuel and food. Diesel price increases affected transportation and agriculture. Fertiliser shortages threatened crop yields. LNG-dependent power systems faced growing stress.

Some governments adopted emergency measures that resembled wartime management rather than ordinary economic policy. Pakistan promoted remote work and reduced commercial hours to curb energy demand. Sri Lanka reintroduced fuel-control mechanisms. Bangladesh restricted non-essential electricity usage. Indonesia imposed purchase limits on transport fuels.

In India, Prime Minister Narendra Modi urged states, industries and citizens to avoid unnecessary energy consumption while accelerating reviews of fuel preparedness and power-system resilience.

At the same time, Asian economies also began falling back on coal to protect electricity systems from LNG shortages. Media reports suggest that coal imports into Japan and South Korea surged sharply as LNG prices climbed more than 60% following the Gulf disruption.

Yet the crisis also triggered a more important strategic shift across Asia.

Several governments accelerated renewable deployment, battery storage approvals and electrification plans almost immediately. Indonesia expanded solar ambitions. India fast-tracked battery and wind approvals. South Korea increased renewable deployment targets. The Philippines moved ahead with solar-plus-storage projects.

Energy think-tanks argue that Asia’s dependence on imported fossil fuels has now become one of the region’s biggest structural economic vulnerabilities, making clean energy deployment increasingly a matter of resilience rather than only decarbonisation.

The rationale was increasingly geopolitical rather than environmental.

Every solar park reduced LNG dependence. Every electric vehicle weakened oil vulnerability. Every battery installation strengthened resilience against imported fossil fuel volatility.

This may ultimately become one of the biggest geopolitical consequences of the Hormuz shock: Asia’s clean energy transition may accelerate not because of climate diplomacy, but because of strategic necessity.

India’s energy dilemma becomes sharper

For India, the crisis carries particularly serious implications.

India imports more than 85% of its crude oil requirements and remains highly dependent on Gulf energy flows. LPG and fertiliser supply disruptions immediately affect households, transport systems and agriculture. Rising oil prices widen the current account deficit and intensify inflationary pressure.

The shipping sector has also come under pressure. Asian bunker fuel shortages caused by Hormuz disruptions are raising freight costs across regional trade routes, threatening broader supply-chain inflation.

But the Hormuz crisis also strengthens India’s strategic case for accelerating domestic clean energy infrastructure.

India already possesses some of the world’s largest renewable energy ambitions. Solar capacity expansion, battery manufacturing, electric mobility, green hydrogen and transmission infrastructure are increasingly central to India’s long-term energy planning.

The economics are changing rapidly.

Every oil shock now improves the relative attractiveness of electrification. Every LNG disruption strengthens the case for storage systems and decentralised power generation. High fossil fuel volatility increasingly acts as an indirect subsidy for renewable deployment.

India’s refining sector also faces an important strategic question. The country has built major refining capacity partly to position itself as a global export hub. But repeated geopolitical disruptions may gradually shift the global conversation from refining dominance towards electrification dominance.

This is particularly relevant as AI-linked electricity demand rises globally. Massive data centre expansion is expected to increase power consumption significantly over the coming decade. Countries able to provide stable, low-cost renewable electricity may gain industrial advantages in attracting digital infrastructure and manufacturing investment.

That dynamic could reshape energy geopolitics itself.

Europe discovers the limits of LNG security

Europe entered the crisis believing it had partially solved its energy vulnerability after reducing dependence on Russian pipeline gas following the Ukraine war.

But the Hormuz shock exposed another uncomfortable reality: replacing pipeline dependence with LNG dependence still leaves economies exposed to global fossil fuel volatility.

Gas prices surged sharply again across European markets as buyers competed for limited LNG cargoes. Electricity prices followed because gas-fired plants continue setting marginal power prices across much of Europe’s electricity system.

Industries once again confronted fears over competitiveness.

Chemical producers, steel manufacturers and fertiliser companies faced rising costs. Governments debated emergency interventions, fuel tax reductions and consumer support mechanisms. Political pressure mounted on climate policies amid fears of another inflationary cycle.

Reports indicate that some European policymakers were already reconsidering parts of the bloc’s climate agenda to soften the economic impact of the energy shock.

Yet unlike the early stages of the Ukraine war, Europe now possesses a stronger renewable buffer.

Renewable deployment since 2022 has reduced part of Europe’s gas exposure. Heat pump adoption has accelerated. Grid integration has improved. Countries such as Spain and Portugal pushed faster renewable permitting and self-consumption reforms. France expanded electrification incentives.

The broader lesson for Europe is becoming increasingly clear: genuine energy security cannot depend indefinitely on imported fossil fuels, regardless of supplier.

The fossil fuel system’s hidden weakness

The Hormuz crisis has reinforced a fundamental structural reality often overlooked in mainstream energy discussions.

Fossil fuel systems are inherently fragile because they rely on uninterrupted daily extraction, transport and combustion.

Oil must continuously flow through pipelines, shipping lanes and refineries. LNG depends on highly complex maritime logistics. Coal, meanwhile, relies on vast mining, rail and shipping networks that are themselves vulnerable to geopolitical disruption and price volatility. Even temporary disruptions rapidly cascade through prices, inflation and industrial production.

Renewable systems operate differently.

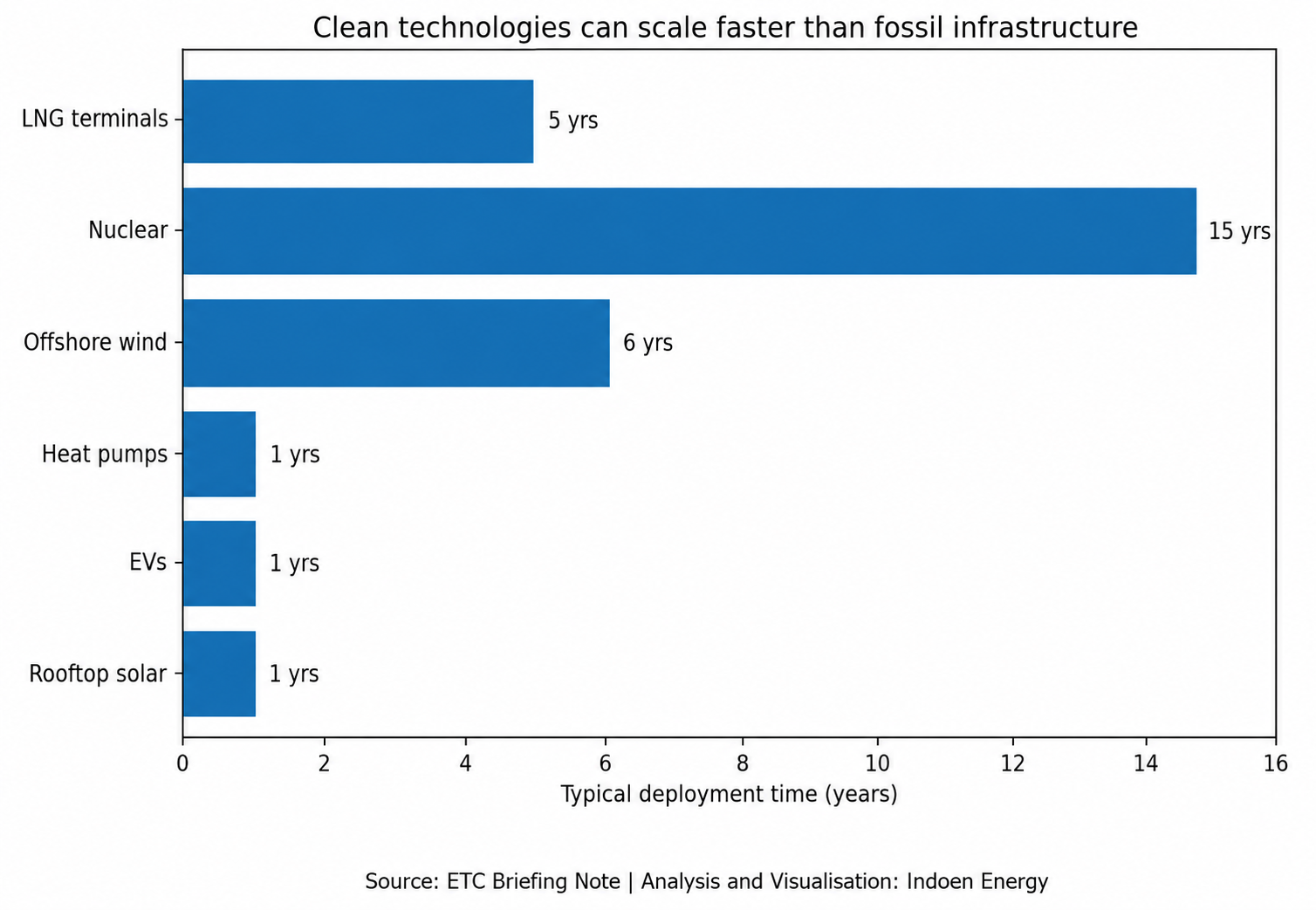

A solar farm in Rajasthan or a wind park in Tamil Nadu does not depend on tanker traffic through the Persian Gulf. Once installed, renewable infrastructure can continue generating energy for decades without requiring constant imported fuel flows.

This distinction matters enormously.

According to the Energy Transitions Commission analysis, clean energy systems are structurally more resilient because most costs are upfront capital investments rather than continuous fuel purchases.

In fossil fuel systems, geopolitical disruptions quickly affect everyday energy supply and prices because the system depends on continuous fuel flows. Electrified systems are different: once solar, wind and battery infrastructure is installed, energy generation becomes far less dependent on constant imported fuel supplies.

That changes how crises propagate through economies.

This does not mean clean energy systems are free from geopolitical vulnerabilities. China dominates large portions of solar manufacturing, battery processing and critical mineral supply chains. The Hormuz crisis itself exposed vulnerabilities in sulphur and metals supply networks essential for battery manufacturing.

But there remains a critical difference between fossil dependence and mineral dependence.

Minerals are embedded in long-lived infrastructure. They can be stockpiled, recycled, substituted and diversified over time. Oil and gas must be consumed continuously every day.

This is why many strategists increasingly argue that clean energy systems, despite their own supply-chain risks, still offer fundamentally greater long-term resilience.

The economics of energy security are being rewritten

Perhaps the most important transformation emerging from the crisis concerns economics rather than climate policy.

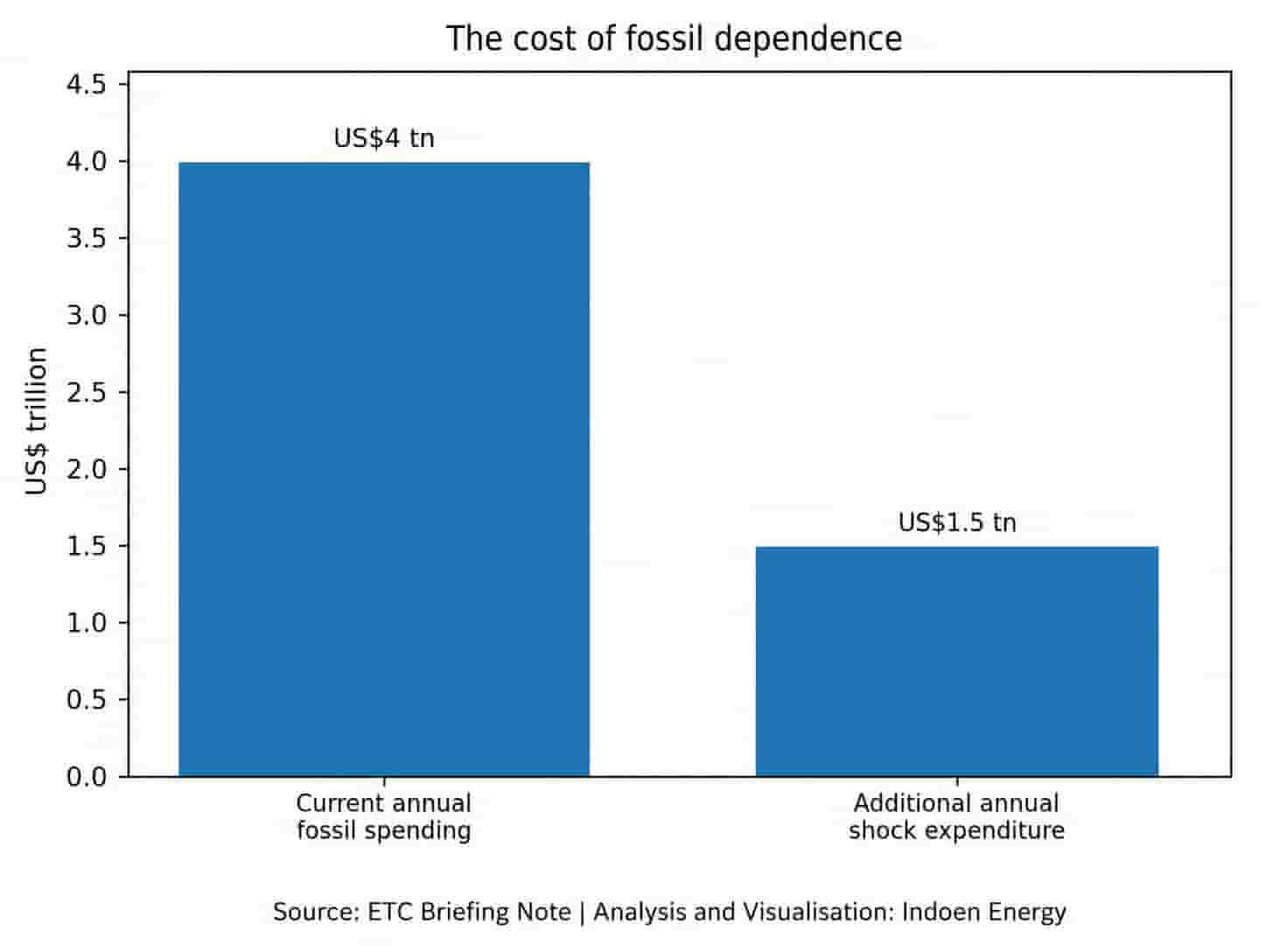

The world already spends trillions of dollars annually on fossil fuels.

“Sustained elevated prices following the Hormuz disruption could add another US$1–2 trillion in annual global expenditure to the world’s current fossil fuel spending of around US$4 trillion.

That additional spending buys essentially the same energy at a higher cost.

By contrast, investments in solar parks, battery systems, EV infrastructure and electricity grids create productive long-term assets that reduce future fuel dependence.

This is beginning to alter political thinking globally.

A senior executive at an Indian clean energy company described the shift bluntly: “Every geopolitical oil shock now becomes free advertising for electrification. Countries are beginning to understand that renewable energy is not only climate policy anymore. It is economic insurance.”

Financial markets appear to be recognising this too.

Chinese solar exports reportedly surged after the crisis intensified. EV demand rose sharply in parts of Europe and Australia. Investors increased exposure to battery manufacturers, transmission companies and storage developers.

Media analyses suggest that although LNG prices have not yet reached the extremes witnessed after Russia’s invasion of Ukraine, the apparent market calm may only be temporary because Europe’s storage refill season and rising Asian summer demand could trigger another wave of price spikes later in the year.

The market may already be anticipating a future where geopolitical instability accelerates the transition rather than slowing it down.

But the transition remains politically difficult

Despite the momentum, the pathway remains messy and contradictory.

Several Asian countries increased coal usage to offset LNG shortages. South Korea delayed coal plant closures. Governments expanded fossil fuel subsidies to manage political pressure. Europe faced calls to soften parts of its climate agenda amid industrial concerns.

These reactions reveal an uncomfortable political truth: governments prioritise immediate stability during crises and that creates a major risk.

Short-term emergency measures can easily become long-term fossil lock-ins. Large LNG infrastructure investments, blanket fuel subsidies and expanded upstream oil projects may provide temporary relief while deepening structural vulnerability for decades.

The challenge therefore is not whether governments respond to the crisis, but how they respond.

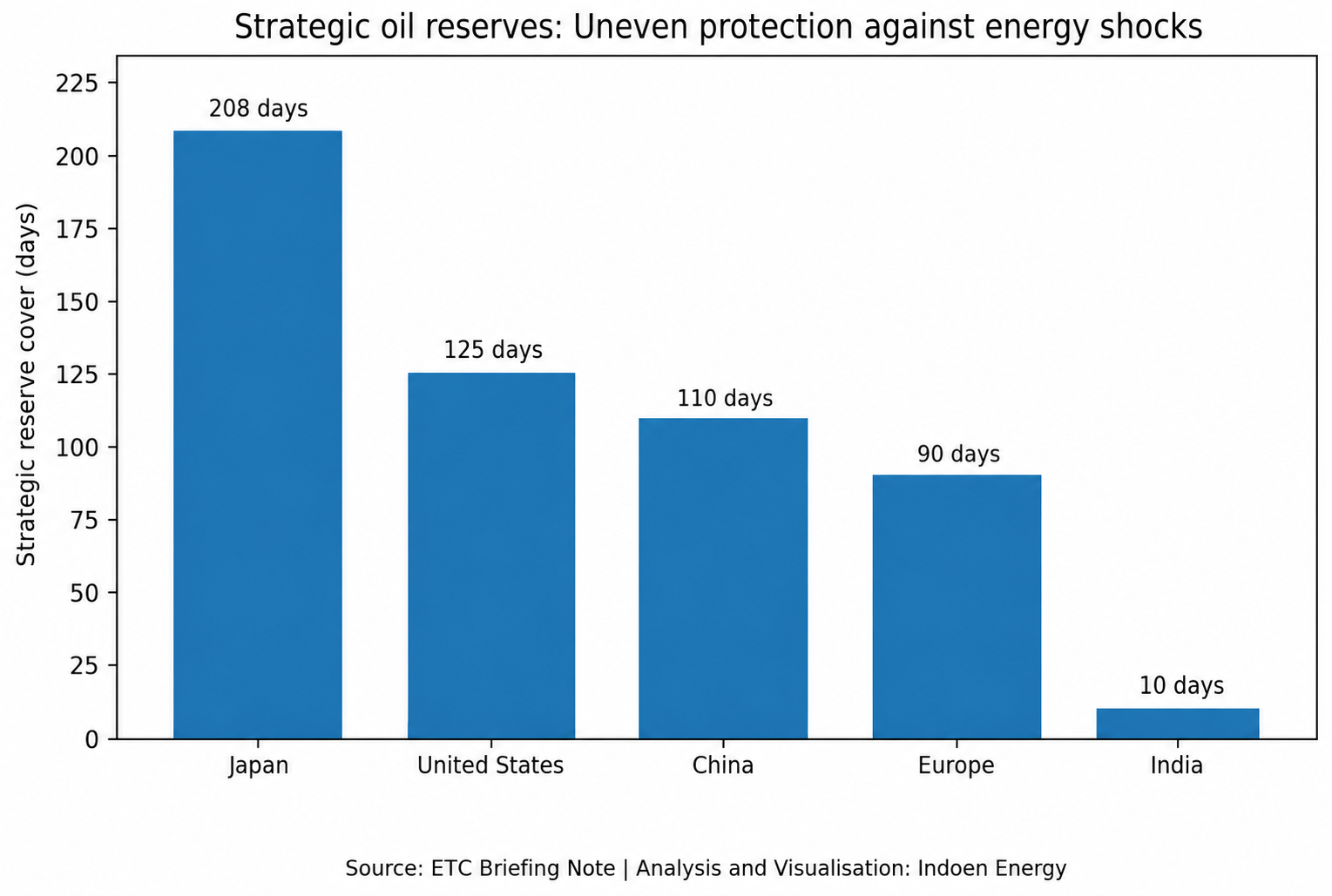

Temporary targeted relief for vulnerable populations may be unavoidable. Strategic reserves remain important. Some short-term fossil fuel adjustments may prove necessary.

But abandoning long-term electrification, efficiency improvements and renewable deployment could ultimately worsen vulnerability rather than solve it.

Gulf capital may finance the next phase of transition

Ironically, some of the biggest beneficiaries of elevated oil prices may become major financiers of the clean energy transition itself.

Gulf sovereign wealth funds are already among the world’s most influential infrastructure investors. Saudi Arabia, the UAE and Qatar have increasingly expanded investments into renewables, hydrogen, grids and global clean technology assets.

The Hormuz crisis may accelerate this trend.

Oil-exporting economies increasingly recognise that recurring geopolitical instability threatens long-term fossil fuel demand growth. Diversifying into energy transition infrastructure therefore becomes both an economic and strategic hedge.

This creates a fascinating paradox.

The very regions whose fossil fuel exports dominate today’s energy system may also help finance parts of the post-fossil energy order.

The age of permanent energy shocks

One of the most unsettling conclusions emerging from the crisis is that such disruptions may no longer be exceptional events.

The world is entering an era where geopolitical fragmentation, climate instability, cyber warfare, resource nationalism and military tensions increasingly overlap.

Energy systems are becoming central battlegrounds in that broader geopolitical environment.

This is why the clean energy transition is increasingly being reframed globally — not merely as an environmental necessity, but as a strategic restructuring of economic power itself.

Countries are no longer investing in renewables only to cut emissions. They are investing to reduce external dependence, stabilise energy costs, protect industrial competitiveness and enhance geopolitical autonomy.

That may fundamentally reshape how energy security is understood in the twenty-first century.

A crisis that may ultimately weaken oil’s strategic power

The irony of the Hormuz crisis is striking.

A disruption rooted in fossil fuel dependence may ultimately accelerate the shift away from fossil fuel systems themselves.

Oil and gas will remain central to the global economy for years. Aviation, shipping, petrochemicals and heavy industry still depend heavily on hydrocarbons. Emerging economies continue requiring affordable energy for development.

But every new geopolitical shock strengthens the economic rationale for electrification.

Every oil price spike increases the attractiveness of EVs.

Every LNG disruption strengthens the case for storage and decentralised renewables.

Every inflationary energy cycle deepens political pressure for stable domestic electricity generation.

The clean energy transition was once driven primarily by climate concerns.

The Hormuz shock is helping transform it into something broader: a strategy for economic resilience in an unstable world.

And that may prove far more powerful.