For much of the past two decades, India’s energy story has been defined by one powerful assumption: demand would keep rising.

Whether it was petrol, diesel, liquefied petroleum gas (LPG), natural gas, electricity, or coal, policymakers and businesses largely planned around a future in which India’s expanding economy would consume ever-increasing quantities of energy.

Recent developments, however, suggest a more complicated picture may be emerging.

As geopolitical tensions in West Asia push oil prices higher, the Indian rupee remains under pressure, and consumers confront elevated energy costs, fresh data indicate that parts of India’s energy economy may already be showing signs of demand destruction — a phenomenon in which sustained high prices begin suppressing consumption itself.

If that trend deepens, the consequences could extend far beyond fuel stations, influencing economic growth, industrial activity, energy investment, and even the pace of India’s energy transition.

The oil shock returns

Global oil markets have once again become hostage to geopolitical risk.

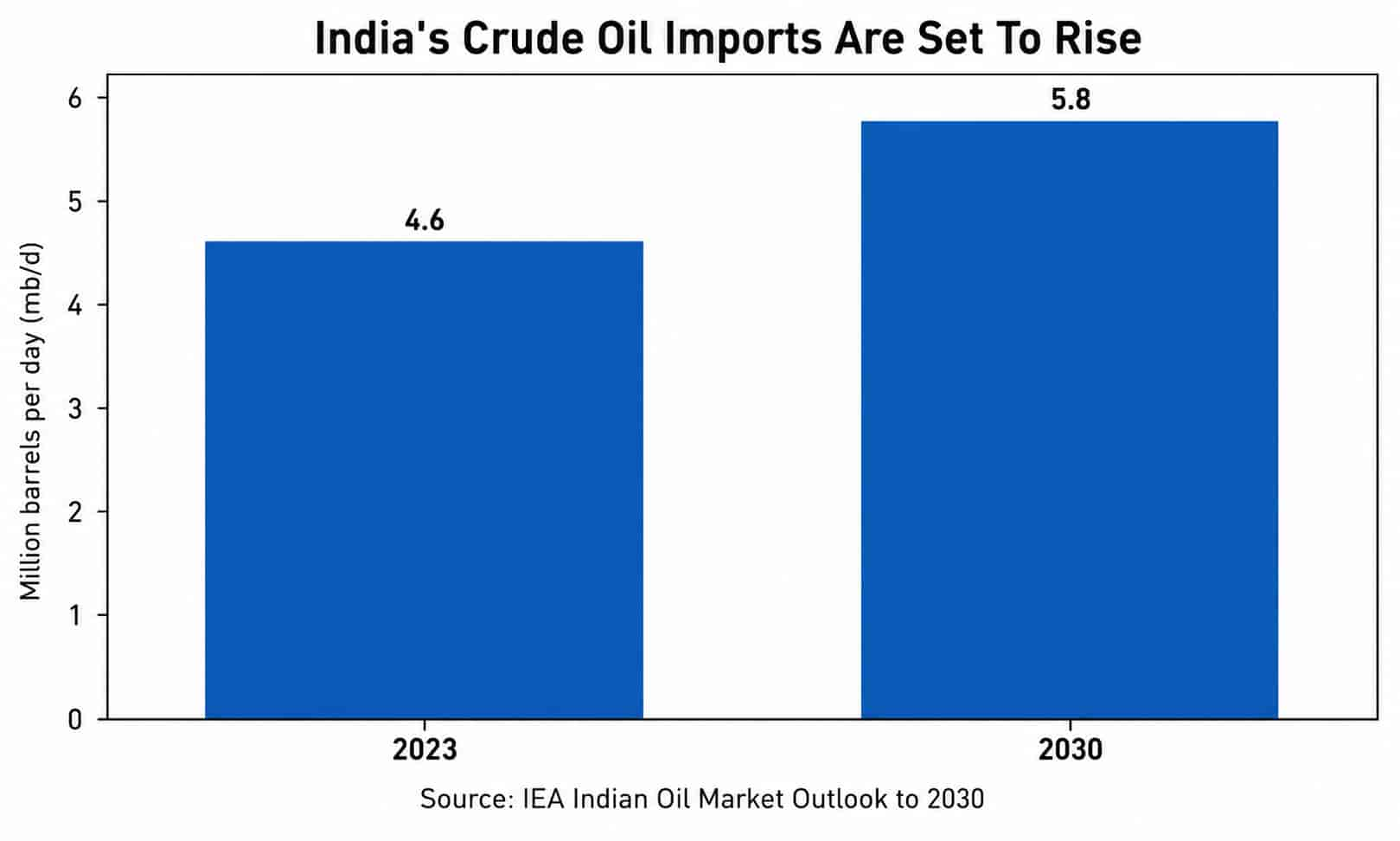

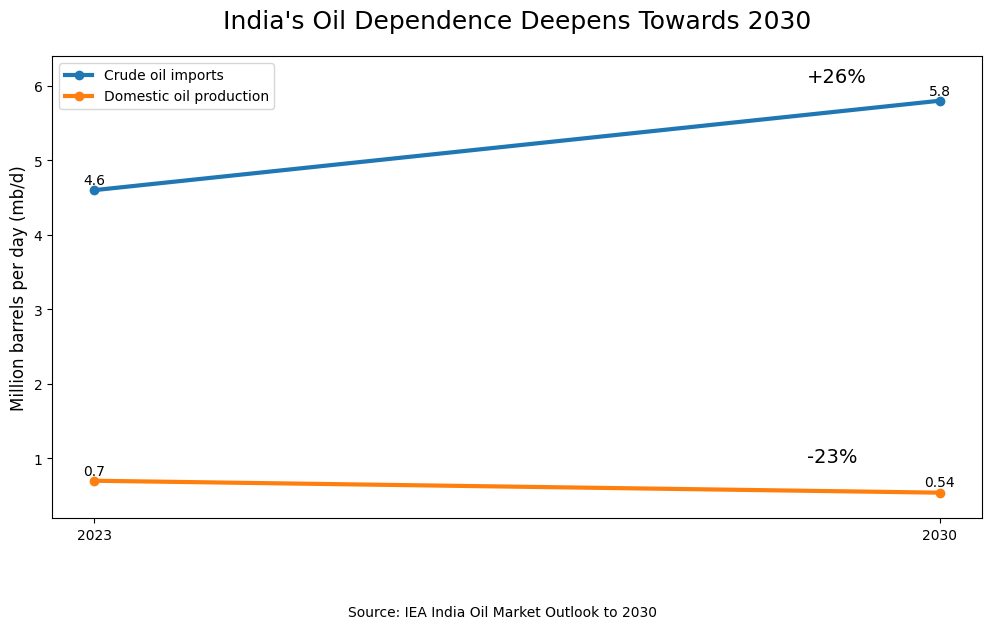

Concerns surrounding potential disruptions in the Strait of Hormuz — the narrow maritime passage through which roughly one-fifth of global oil supplies move — have revived fears of supply shortages and price spikes. The issue carries particular significance for India, which imports more than 85% of its crude oil requirements and remains one of the world’s largest energy importers.

As Indoen Energy previously noted in its analysis of growing West Asian risks, India’s energy security remains deeply intertwined with developments far beyond its borders.

Recent warnings from the Reserve Bank of India suggest that a sustained rise in oil prices could weaken economic growth, increase inflationary pressures, and complicate monetary policy decisions.

The challenge is magnified by currency movements. The Indian rupee has weakened against the US dollar during periods of energy market stress, increasing the effective cost of imported crude even when benchmark oil prices remain stable.

Analysts at ING have warned that higher oil prices could place additional pressure on the rupee and widen India's external vulnerabilities

For an economy importing hundreds of billions of dollars worth of energy products annually, the combination of higher oil prices and a weaker currency creates a double burden.

A surprising signal from fuel demand

Ordinarily, rising energy consumption is viewed as a sign of economic expansion.

Yet recent petroleum planning data suggest that India’s fuel demand fell by around 4.6% year-on-year during a recent reporting period. Natural gas consumption declined by approximately 16.7%, while LNG imports reportedly plunged by nearly 30%.

Viewed in isolation, such movements could reflect seasonal factors, weather patterns, or temporary market adjustments.

Taken together, however, they raise an important question.

Are consumers and industries beginning to reduce energy consumption because prices have become too high?

The concept is well known in commodity markets. When energy costs rise sharply, households reduce discretionary travel, logistics companies optimise routes, industries postpone production, and businesses seek efficiency gains.

The result is demand destruction.

Historically, major oil shocks have often contained the seeds of their own reversal because sufficiently high prices eventually suppress consumption.

The difference today is that demand destruction may no longer be merely cyclical. In some sectors, it may be becoming structural.

The LNG warning

Perhaps the most underappreciated signal lies in natural gas markets.

India has spent years promoting gas as a transition fuel capable of reducing coal dependence while supporting industrial growth and urbanisation.

Yet imported LNG remains highly exposed to international pricing volatility.

Following the disruptions triggered by the Russia-Ukraine conflict, global LNG prices experienced unprecedented spikes. Although prices have moderated from their peaks, many industrial consumers remain sensitive to future volatility.

The recent decline in LNG imports may therefore reflect more than temporary weakness.

It could indicate that portions of Indian industry are becoming reluctant to rely heavily on imported gas when cheaper or more predictable alternatives remain available.

This presents policymakers with a dilemma. Natural gas is frequently positioned as a bridge fuel in decarbonisation strategies, but its attractiveness diminishes when geopolitical disruptions repeatedly trigger price instability.

The economic ripple effect

The implications extend well beyond the energy sector.

Bloomberg recently highlighted concerns that higher oil prices could threaten India’s stock market rebound by increasing inflation expectations and reducing corporate profitability.

Transport-intensive industries, aviation, chemicals, fertilisers, logistics operators, and manufacturing firms all face higher input costs when energy prices rise.

Meanwhile, governments face difficult choices regarding fuel pricing. Reports suggest policymakers may eventually face pressure to adjust domestic fuel prices if elevated crude prices persist alongside a weaker rupee.

Allowing domestic fuel prices to rise can help protect public finances but risks reducing consumption and weakening economic activity. Absorbing the shock through subsidies or tax reductions can support demand but places pressure on fiscal balances.

India has confronted this trade-off repeatedly over the past decade.

The difference now is that global energy volatility appears increasingly persistent rather than episodic.

The hidden accelerator of the energy transition

Paradoxically, the same oil shock that threatens growth may also accelerate India's long-term energy transition.

One of the most striking developments in recent months has been the growing momentum behind battery storage investments, renewable energy deployment, and grid modernisation initiatives.

Reliance Industries, for example, has begun operationalising battery energy storage system (BESS) capacity, signalling that large-scale storage is moving from ambition to implementation.

This creates a powerful feedback loop.

Every major oil shock strengthens the economic argument for electrification.

Every episode of LNG volatility strengthens the case for domestic renewable generation.

Every disruption in maritime oil routes increases interest in technologies that reduce import dependence.

As Indoen Energy recently explored in its analysis of global oil market fragmentation, geopolitical instability is increasingly becoming an energy transition driver rather than merely an energy security concern.

A global phenomenon

India is not alone.

Europe’s response to the energy crisis triggered by Russia’s invasion of Ukraine demonstrated how rapidly high fossil-fuel prices can alter investment decisions.

Solar deployment accelerated. Heat pump adoption increased. Battery manufacturing received unprecedented policy support.

In China, concerns surrounding energy security have reinforced investments in electric vehicles, battery manufacturing and renewable energy supply chains. Even recent discussions around potential disruptions in the Strait of Hormuz have highlighted the degree to which major Asian economies remain vulnerable to imported oil routes.

The result is one of the most intriguing dynamics in global energy markets.

High fossil-fuel prices initially strengthen revenues for producers but often accelerate the technologies that eventually weaken fossil-fuel demand.

The process is slow, uneven, and frequently overlooked. Yet history suggests it can reshape entire energy systems.

What happens next?

Whether India is genuinely entering an era of demand destruction remains uncertain.

A temporary decline in fuel consumption does not automatically signal a structural shift.

Economic growth remains robust by international standards. Rising incomes, urbanisation, expanding transport networks, and industrialisation continue to support long-term energy demand growth.

However, the emerging signals deserve attention.

If future oil shocks repeatedly coincide with rupee weakness, industrial cost pressures and consumer caution, demand growth could become less predictable than many forecasts assume.

The bigger story may not be that India consumes less energy. It may be that India begins consuming energy differently. That distinction matters.

For decades, policymakers worried primarily about securing enough fuel to meet rising demand. Increasingly, the challenge may involve ensuring that demand growth itself does not become vulnerable to volatile global commodity markets.

In that sense, the hidden cost of the latest oil shock is not merely higher fuel bills.

It is the possibility that energy affordability, rather than energy availability, becomes the defining constraint on India’s next phase of economic growth.