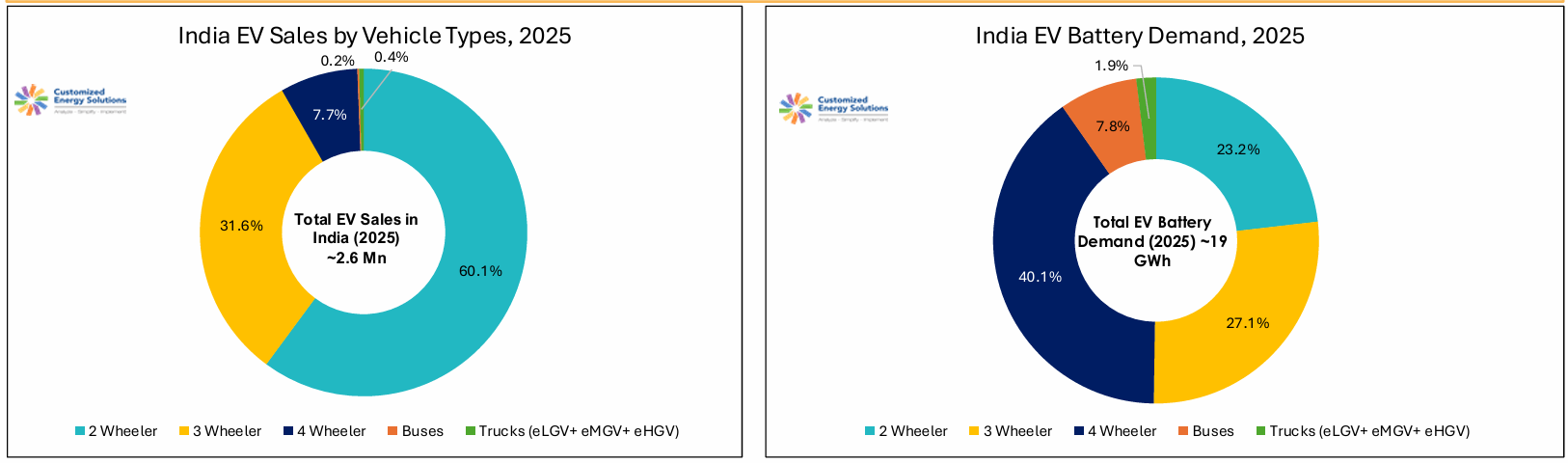

According to a new report from the India Energy Storage Alliance, India's EV sales rose from 2.0 million units in 2024 to roughly 2.6 million in 2025, a 26% increase that outpaced global EV sales growth of 20%.

Two-wheelers and three-wheelers together made up over 91% of that volume, while four-wheelers, though still a modest 7.7% share, are described as entering a genuine growth phase.

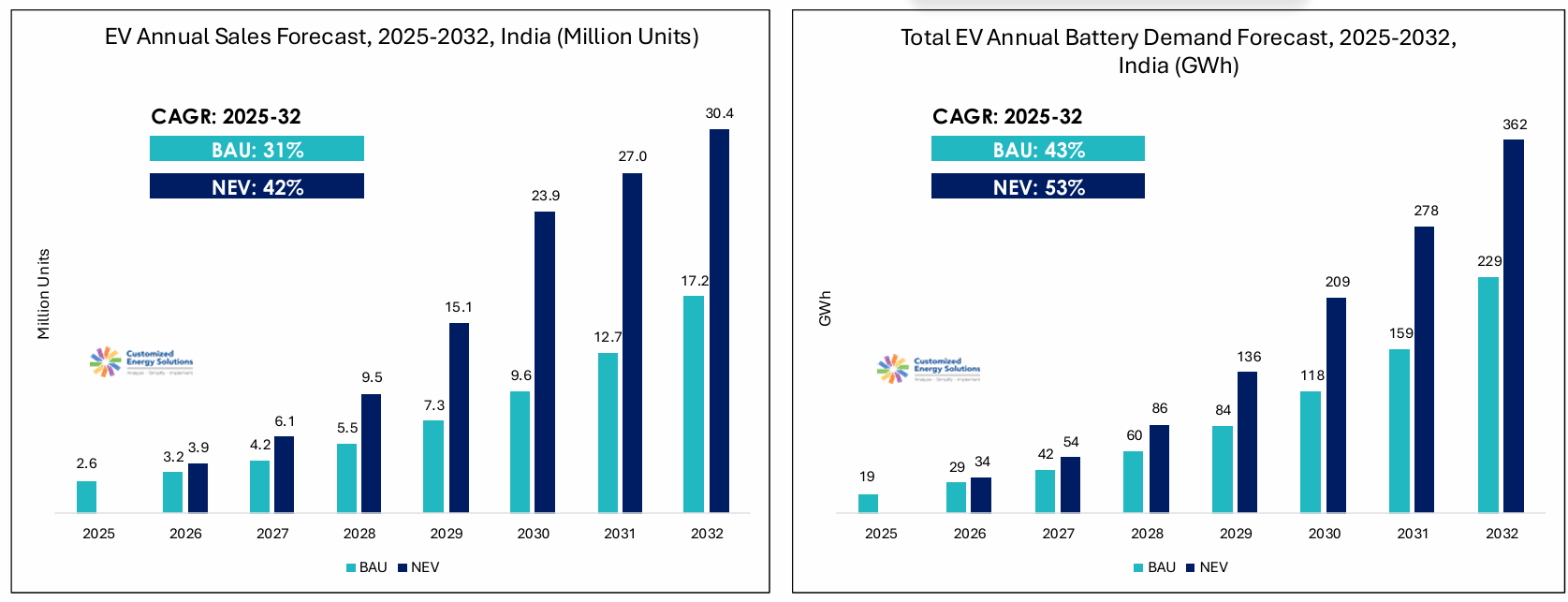

The report's forecasts diverge sharply depending on policy execution.

Under a business-as-usual trajectory, annual EV sales would reach 17.2 million units by 2032. Under a "National EV Target" scenario, premised on full delivery of the PM E-Drive scheme's outlay and NITI Aayog's 2030 penetration goals, sales could hit 30.4 million units, a twelvefold increase from 2025.

Battery demand would follow a similar curve, climbing from 19 GWh in 2025 to as much as 362 GWh in the higher-growth scenario.

The localisation gap

The report's most striking finding concerns where the value in this expansion actually accrues. Battery packs alone account for around 52% of India's EV components market, making them the single largest cost item in any electric vehicle.

Yet battery pack localisation stands at just 10–20%, the lowest of any major component category. Inverters fare only slightly better at 22% localised content, also flagged as "critical" in the report's assessment.

By contrast, traction motors and battery management systems show comparatively higher domestic content, at 35% and 28% respectively, reflecting their lower capital intensity and heavier reliance on software rather than cell chemistry or power semiconductors.

"The imbalance in localisation tells you where India's real EV competitiveness challenge lies," said a policy adviser familiar with the sector. "It isn't in selling vehicles. It's in owning the technology inside them."

Batteries and power electronics combined account for an estimated 50–60% of total EV cost, according to the study, meaning that India's current import dependence for cells and semiconductors leaves domestic manufacturers with limited control over pricing during global supply disruptions or raw material price spikes.

Where the incentives are going

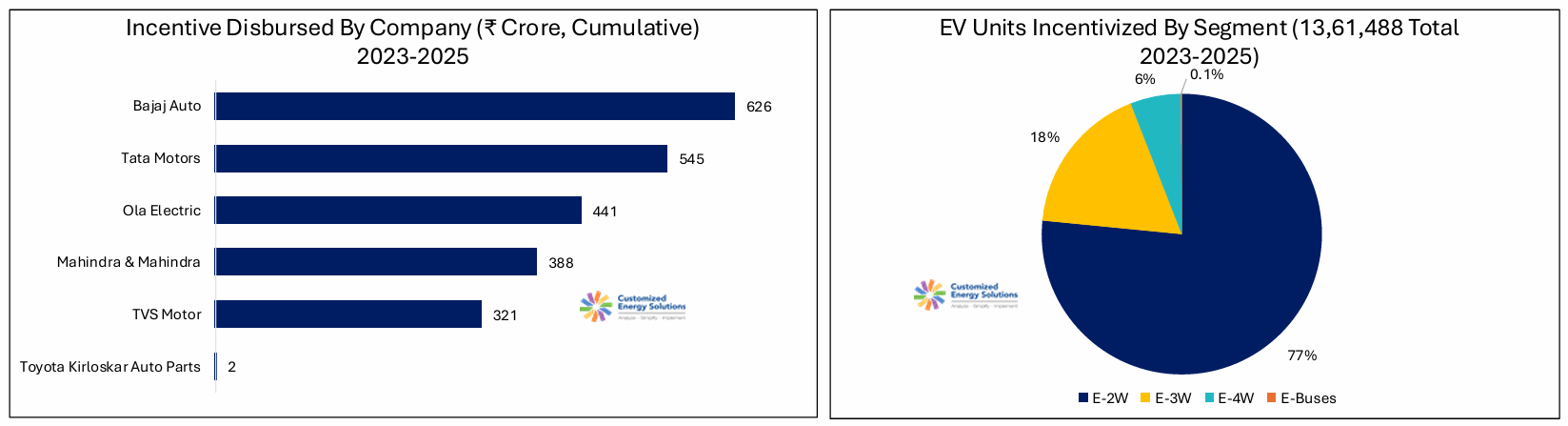

Government support through the Auto PLI scheme illustrates a related concentration problem. Of the ₹25,938 crore ($269 million) cabinet-approved outlay, only ₹2,322 crore ($241 million) had been disbursed as of December 2025, against ₹35,657 crore ($370 million) of investment made to date.

Nearly 99.9% of that incentive money has gone to just five vehicle manufacturers, Bajaj Auto, Tata Motors, Ola Electric, Mahindra & Mahindra and TVS Motor, while component manufacturers have received what the report describes as a negligible share.

Bajaj Auto led disbursements at ₹626 crore ($65 million), followed by Tata Motors at ₹545 crore ($57 million) and Ola Electric at ₹441 crore ($46 million). Toyota Kirloskar Auto Parts, by contrast, received just ₹2 crore (roughly $208,000), underscoring how thinly the scheme's benefits have reached the component-manufacturing side of the industry that the report identifies as central to long-term cost competitiveness.

A fragmented policy map

Adding to the complexity, EV policy support varies widely by state, split between what the report terms "fiscal aggression leaders" and "regulatory maturity leaders." Maharashtra's 2025–2030 EV policy carries a ₹1,993 crore ($207 million) budget, a 114% increase over its predecessor, offering up to ₹20 lakh (roughly $21,000) per electric bus and mandating EV-ready parking in all new residential buildings.

Delhi's draft 2.0 policy combines subsidies of ₹10,000 ($104) per kWh, capped at ₹30,000 ($312), with a ban on new petrol two-wheeler registrations from April 2028.

Karnataka has taken a manufacturing-first approach instead, allocating ₹3,400 crore ($353 million) to battery energy storage systems and establishing EV manufacturing clusters at Dharwad and Gauribidanur.

"States are effectively running two different experiments simultaneously, one built on subsidies, the other on mandates," an analyst at a leading energy research institution observed. "Which model proves more durable will shape investment decisions well beyond this decade."

The road ahead

The report's own analysis suggests traction motors, unlike batteries, tend to last around 15 years and are rarely replaced outright, with lifecycle maintenance instead driven by repair of bearings, insulation and cooling elements.

That longevity may partly explain why domestic players such as Bharat Forge, Bosch India, Uno Minda and Tata AutoComp are now pushing into e-axles and power electronics, seeking to capture value in components that will need servicing for over a decade, even as battery cell technology continues to evolve.

Readers following India's parallel effort to reduce import dependence in other clean-technology segments may find useful context in Indoen's Energy’s earlier coverage of the country's cleantech manufacturing gamble, which examines a comparable localisation dilemma in solar and battery storage.

Whether India closes its EV components gap will depend, per the report's findings, on continued battery cost reductions, full execution of PM E-Drive and PLI commitments, and reduced dependence on critical mineral imports. The market's scale is no longer in question; whether India captures its value is.

Follow us on : X | LinkedIn | Facebook | Bluesky