When conflict broke out in the Middle East at the end of February 2026, few analysts expected the fallout to reach as far as it has. The Strait of Hormuz, which carried close to a fifth of the world's LNG cargoes before the war, was effectively closed to shipping for four months.

QatarEnergy halted production at its Ras Laffan complex, the world's largest liquefaction facility, after military strikes on 18-19 March damaged two trains with a combined capacity of 17.5 billion cubic metres (bcm) a year. The United Arab Emirates fared little better, with its Habshan gas processing complex running at roughly 60% capacity for months.

The scale of the disruption is striking. Qatar's gas production is estimated to have collapsed by almost 75% year-on-year between March and June, while combined Qatari and Emirati LNG supply is forecast to fall by around 45%, or 55 bcm, for 2026 as a whole.

An interim US-Iran agreement reached in mid-June has allowed a cautious rise in tanker traffic through the Strait, but volumes remain a fraction of pre-war levels, and the report's forecast assumes a full reopening only by the third quarter, with Gulf production not normalising until early 2027.

Markets absorbed the shock, but not without scars

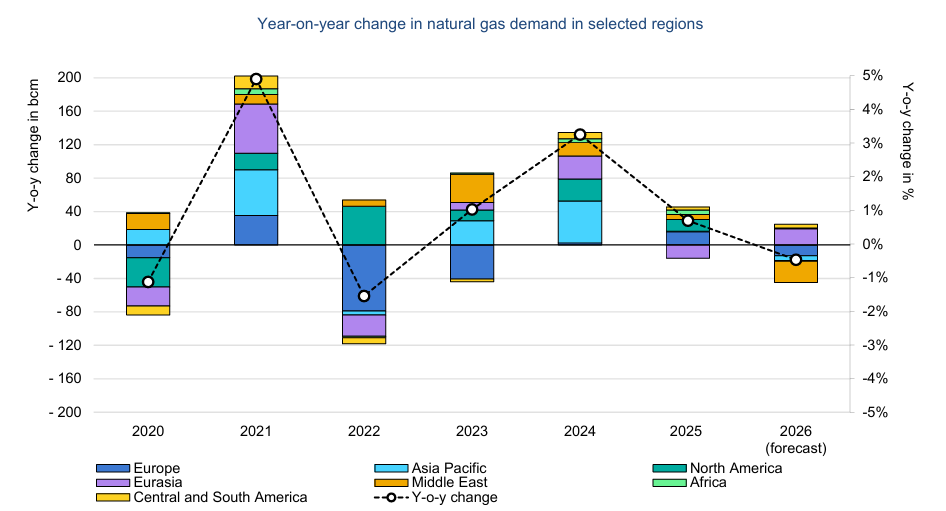

What makes this crisis distinctive is how much of the shortfall the rest of the world managed to plug. New liquefaction capacity in North America and Africa, alongside stronger output from legacy plants in Russia, Nigeria and Malaysia, offset roughly three-quarters of the lost Gulf volumes between March and June.

Global LNG production fell by only 4% over that period, a remarkably contained outcome given that a fifth of global supply had effectively vanished overnight.

Prices told a different story. European TTF and Asian spot LNG benchmarks both hit their highest second-quarter averages since 2022, with Asian prices rising 45% year-on-year to around US$17.5 per million British thermal units.

The premium Asian buyers were paying over European hubs flipped from roughly 90 cents in January to more than US$2 from March onward, a wow-factor detail that captures just how sharply Asia bore the brunt of the crisis, pulling flexible cargoes away from Europe even as European storage entered the year already 13% below normal.

"The speed with which non-Gulf supply absorbed the shock surprised even seasoned traders, but price volatility of this magnitude tells you the market was never truly comfortable with the loss," said an analyst at a leading energy research institution.

India's rationing moment

India's exposure to the crisis has been direct and, at times, severe.

Within days of the Strait's closure, the government invoked the Natural Gas (Supply Regulation) Order 2026, diverting gas to residential and CNG users while curbing supplies to fertiliser plants, industry and refineries.

Fertiliser production fell by 7% year-on-year between January and April, petrochemical output contracted by 21%, and gas-fired power generation dropped by 17% in the first half of the year, even as coal-fired generation rose by 4% — a clear instance of gas-to-coal switching playing out in real time.

Yet the aggregate LNG import picture proved more resilient than the domestic rationing might suggest. India's LNG imports actually rose by around 1% year-on-year in the period, as deliveries from Africa almost tripled and North American cargoes increased by 70%, more than compensating for a 40% drop in Middle Eastern supply.

That diversification is arguably the report's most encouraging finding for Indian policymakers: it demonstrates that alternative sourcing routes, painstakingly built up over recent years, can be mobilised quickly under stress. India formally lifted its emergency gas allocation order on 4 July, though the report still expects the country's full-year gas demand to decline by around 8%, one of the steeper contractions among Asian importers.

This aligns with concerns Indoen Energy has flagged before over the durability of India's gas ambition, where reform momentum and supply security have often pulled in different directions.

Fertiliser markets feel the second-order shock

Beyond direct energy costs, the conflict has driven a less visible but arguably more consequential crisis in global fertiliser supply.

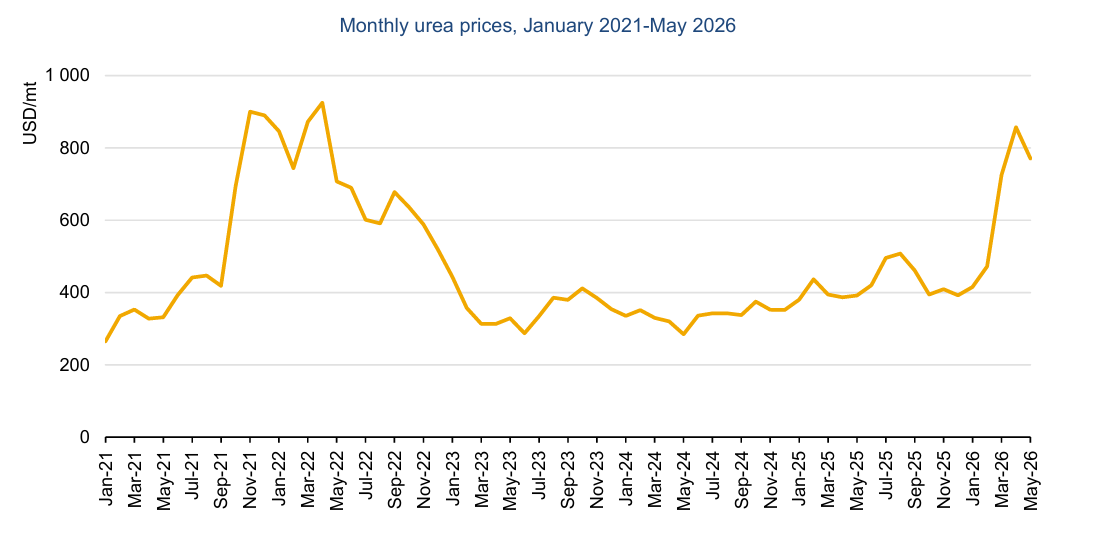

The Gulf accounts for around a quarter of global seaborne urea and half of seaborne sulphur trade, and the halt in these shipments pushed urea prices to near US$800 a tonne between March and May, their highest since the 2022 gas shock, while sulphur prices surged more than fivefold.

For India, where fertiliser plants were designated a priority sector yet still saw gas deliveries fall by 15% in March and April, the risk is that the effects of an energy crisis thousands of kilometres away are transmitted directly into farm input costs, with the added complication of a possible El Niño-driven drought later in the year.

A tighter market for longer than expected

Perhaps the most consequential finding buried in the report's data is the medium-term one: cumulative LNG supply losses between 2026 and 2030 are now estimated at 140 bcm, equivalent to 15% of all new global supply expected over that period.

Qatar's damaged liquefaction trains alone could take three to five years to repair, and its flagship North Field East expansion, previously due online in the second half of 2026, may now be delayed by more than a year. That timeline matters enormously for import-dependent economies like India that had been counting on this wave of Qatari supply to ease prices later in the decade.

Not every reading of the data points to permanent tightness, however. LNG carrier ordering has accelerated sharply even as freight rates ease, suggesting shipowners still expect medium-term demand growth once new liquefaction capacity, concentrated heavily in the United States, comes fully online after 2027.

"Markets are pricing in a temporary squeeze rather than a structural shortage, but the next eighteen months will be uncomfortable for import-dependent buyers," noted a policy adviser familiar with the sector.

The road ahead

With global gas demand now forecast to contract by 0.5% in 2026 — its third annual decline this decade — and the Middle East itself facing its first drop in gas consumption since 1993, the crisis has inverted assumptions that underpinned energy planning across Asia.

For India, the lesson is less about any single shortfall and more about the value of diversified sourcing, flexible fuel-switching capacity, and a fertiliser and power sector that can absorb shocks without triggering wider economic damage. Whether that resilience holds if the Strait's reopening slips again remains, for now, an open question.

Follow us on : X | LinkedIn | Facebook | Bluesky