When US President Donald Trump announced a ceasefire agreement with Iran on 15 June 2026 — authorising the ‘toll free’ passage of ships through the Strait of Hormuz — oil prices fell immediately, and India's petroleum ministry officials exhaled.

The relief was entirely justified. For roughly three and a half months, beginning in late February, India had scrambled to reroute, renegotiate, and reimagine its crude oil supply chain after Iranian threats restricted transit through the world's most critical oil corridor.

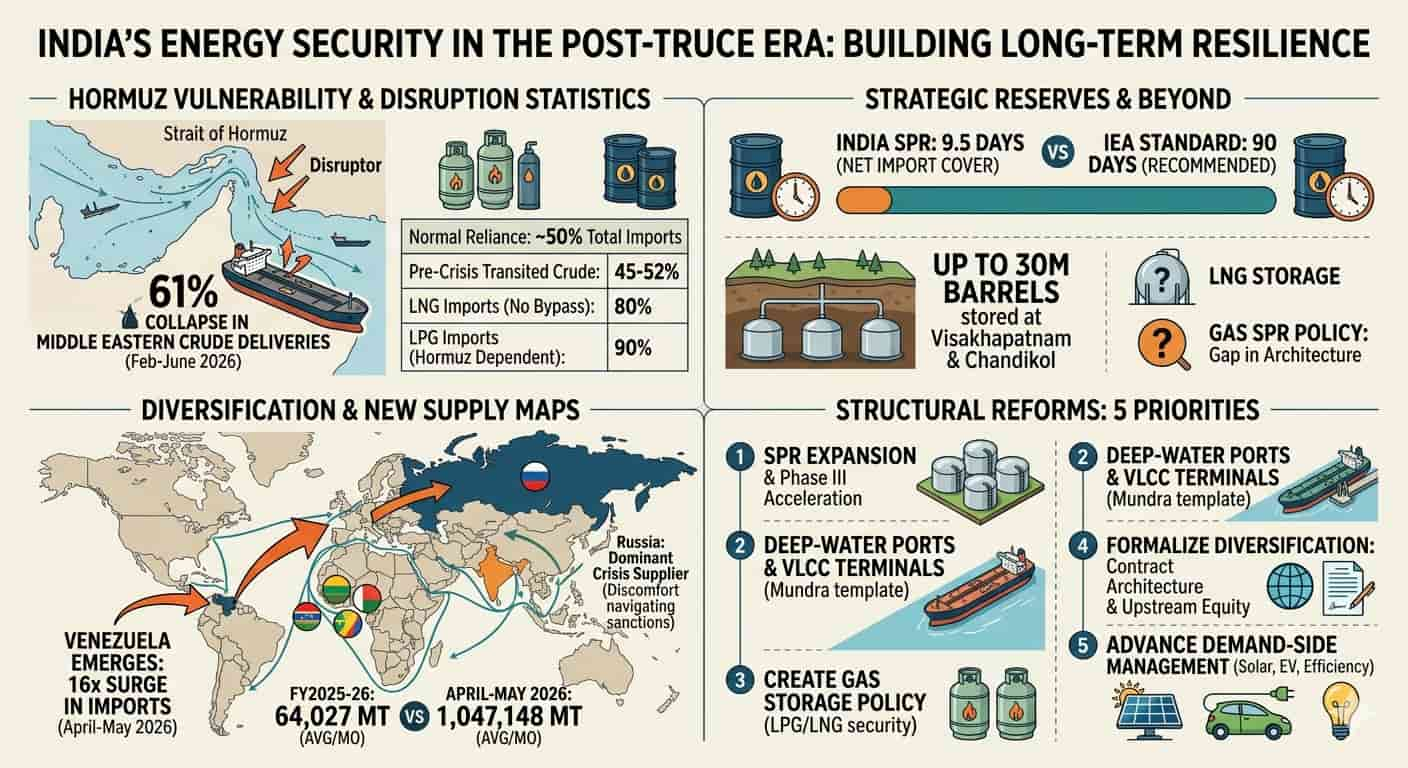

Middle Eastern crude deliveries to India — normally accounting for roughly half of the country's total import volume — had collapsed by an estimated 61%, forcing refineries to absorb discounted Russian barrels, pursue emergency Venezuelan spot purchases, and activate a naval escort operation, Operation Urja Suraksha, to protect Indian-flagged vessels in the Arabian Sea.

But energy experts, refinery officials, and supply chain analysts are warning that the morning after the truce carries its own set of dangers. Chief among them: the assumption that reopening Hormuz restores energy security to the level that existed on 27 February 2026 — the day before the crisis — ignores the fact that what existed before was itself insufficient.

"The ceasefire removes the immediate fire, but the kindling hasn't changed," a senior official at a state-run Indian refinery told Indoen Energy. "Our reserve position, our port infrastructure, our over-dependence on a single maritime corridor — none of that is fixed because the Americans and Iranians reached a deal."

The numbers that lay bare the vulnerability

India imports more than 88% of its crude oil requirements, consuming approximately 5 million barrels per day (bpd). Before the Hormuz crisis, an estimated 45–52% of that volume transited the Strait, with Iraq, Saudi Arabia, the UAE, Kuwait, and Qatar serving as the dominant suppliers. Another 80% of India's LNG imports and roughly 90% of its LPG imports moved through the same passage.

The financial implications of any sustained disruption are staggering: approximately US$3.4 trillion in annual trade flows through the Strait of Hormuz globally, and even partial restrictions are enough to trigger immediate price spikes in freight, insurance, and cargo costs.

The financial implications of any sustained disruption are staggering: approximately US$3.4 trillion in annual trade flows through the Strait of Hormuz globally, and even partial restrictions are enough to trigger immediate price spikes in freight, insurance, and cargo costs.

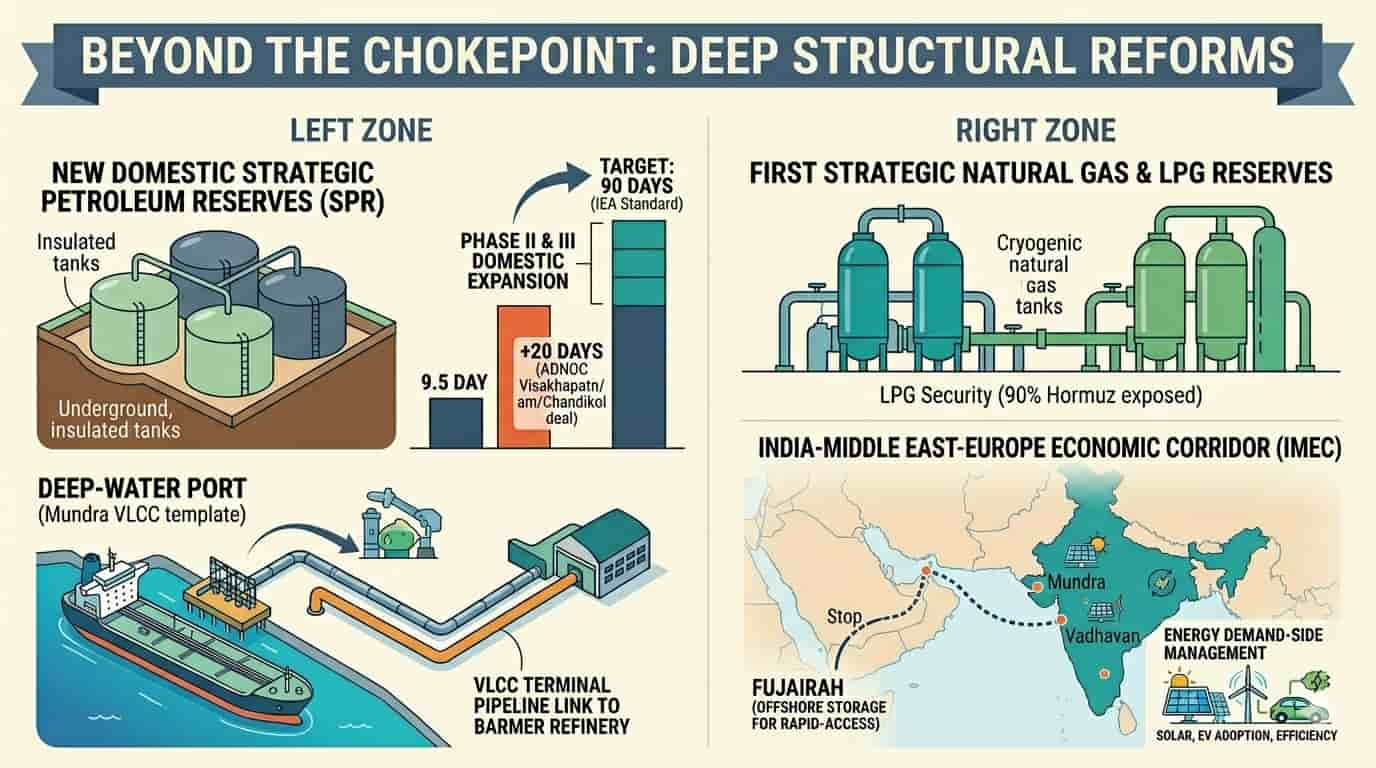

India's strategic petroleum reserve (SPR) — the country's buffer against such shocks — provides only 9.5 days of net import cover, a figure that has drawn sustained criticism from energy security analysts. The International Energy Agency recommends a 90-day strategic reserve benchmark for its member states; India holds barely a tenth of that standard.

While state-run oil companies maintain additional commercial stocks of crude and petroleum products equivalent to roughly 64.5 days of net imports, those buffers are designed for commercial use and are not entirely available for emergency drawdown in the way strategic reserves are.

During the Hormuz crisis, those numbers came under severe pressure. With combined crude and SPR stocks, India had an effective buffer of only 40–45 days of Hormuz-transiting imports under disruption conditions — far short of what analysts had hoped.

And crucially, India has no strategic reserves for natural gas at all, leaving the LNG and LPG segments almost completely exposed. As Indoen Energy reported earlier this year, LNG supplies from Qatar and the UAE, which together account for more than 56% of India's US$14.8 billion LNG import bill in 2024–25, move exclusively through Hormuz under long-term contracts that offer no geographic bypass provision.

The normalisation delay that experts warned about

Energy experts quoted in several media reports have cautioned that even with a formal ceasefire in place, oil supply normalisation through Hormuz could take months. Shipping and insurance markets, tanker operators, and port agents do not snap back the moment a political announcement is made.

Insurers will need to reassess war-risk premiums. Tanker operators will recalibrate routing decisions. Gulf producers, whose own export infrastructure was partially disrupted during the crisis — the UAE's ADNOC, for instance, could produce only 2.02 million bpd during peak disruption, against its rated capacity of 4.2 million bpd — will need time to restore output discipline.

India's crude oil basket price had surged to above US$114 per barrel at its peak during the crisis from US$69 per barrel before the disruption. While prices fell sharply on the ceasefire announcement, market participants noted that the structural conditions that drove that spike — thin insurance capacity for Gulf-transiting vessels, fragile freight markets, a scramble among Asian buyers for non-Hormuz alternatives — had not materially changed.

"The commercial machine takes longer than the political machine to restart," a Mumbai-based shipping and energy logistics consultant observed. "Indian refineries have already locked in Russian, Venezuelan, and West African cargoes for July and August. That crude will arrive regardless of what happens at Hormuz. The Middle Eastern grades will take another quarter, at least, to return to their pre-crisis share."

The crisis that revealed an architecture problem

The deeper lesson of the 2026 Hormuz crisis is not that India was unlucky. It is that India was structurally exposed in ways that pre-crisis assessments consistently underplayed.

The country's Hormuz dependency had actually been rising in the months before the crisis: Russian crude's share of India's imports had declined from 33% in mid-2025 to around 20% by early 2026, as Indian refiners reacted to tightening US sanctions on Russian producers, including the November 2025 designations of Rosneft and Lukoil.

That pullback from Russia had increased India's reliance on Middle Eastern grades, pushing its Hormuz exposure from 41% in 2025 to 52% by February 2026.

That pullback from Russia had increased India's reliance on Middle Eastern grades, pushing its Hormuz exposure from 41% in 2025 to 52% by February 2026.

The Atlantic Council, writing during the crisis, argued that the durable structural fix lay in two interconnected investments: expanding India's ability to receive and store non-Hormuz supply at scale, and developing the long-haul maritime logistics partnerships with the Americas and West Africa that make those investments commercially viable.

India's first VLCC terminal at Mundra port, inaugurated by Adani Ports in January 2026, was a step in this direction: designed to handle very large crude carriers with capacities exceeding 300,000 DWT, the terminal connects via a 489 km pipeline to HPCL's Rajasthan refinery at Barmer. But a single terminal — even a world-class one — cannot substitute for a comprehensive non-Hormuz supply architecture.

The critical question analysts are now asking is whether the ceasefire will reduce the political urgency that, at the height of the crisis, was finally translating into action.

History offers little comfort. After every major Hormuz scare — in 2011–12, in 2019, and during the early Red Sea crisis of 2023–24 — India undertook emergency reviews of its energy security architecture, commissioned feasibility studies on SPR expansion, and discussed deepening non-Gulf supply chains. Each time, once crude prices normalised, the urgency dissipated.

India's new oil map: A scramble that exposed structural creativity

The scramble itself, while painful, revealed an important and under-discussed dimension of India's energy geography: the country's refinery configuration, built over decades to process heavy, sour, discounted crude, has become an inadvertent strategic asset.

Indian refineries can handle Venezuelan extra-heavy crude, discounted Russian Urals, and African grades that Western European refineries reject or downgrade. This technical flexibility, combined with India's position as the world's third-largest crude consumer, gives it negotiating leverage that smaller or less diversified importing nations simply do not possess.

Venezuela's emergence as one of India's top three crude oil suppliers in April and May 2026 illustrated this dynamic. India's average monthly imports from Venezuela surged from 64,027 metric tonnes during the whole of FY 2025–26 to 1,047,148 metric tonnes during April–May of FY 2026–27, an increase of more than 16 times in a single quarter.

Petroleum Minister Hardeep Singh Puri met Venezuela's Acting President Delcy Rodríguez in New Delhi on 4 June 2026 to formalise the strategic dimension of what had begun as a crisis-driven spot relationship. A technical team is now being dispatched to Caracas to explore upstream collaboration in a country that holds the world's largest proven oil reserves.

Media reports suggest that the discussions also covered critical minerals, suggesting India views Venezuela as a potential partner in the energy transition as well as in conventional oil.

On the Gulf side, Prime Minister Narendra Modi's visit to the UAE on 15 May 2026 produced a landmark storage agreement: ADNOC and the Indian Strategic Petroleum Reserves Limited (ISPRL) signed an MOU under which up to 30 million barrels of ADNOC crude will be stored in India's SPR network, including at Visakhapatnam in Andhra Pradesh and at a new facility at Chandikol in Odisha.

On the Gulf side, Prime Minister Narendra Modi's visit to the UAE on 15 May 2026 produced a landmark storage agreement: ADNOC and the Indian Strategic Petroleum Reserves Limited (ISPRL) signed an MOU under which up to 30 million barrels of ADNOC crude will be stored in India's SPR network, including at Visakhapatnam in Andhra Pradesh and at a new facility at Chandikol in Odisha.

This represents a near-fivefold increase from the 5.86 million barrels ADNOC currently holds at Mangalore. Perhaps more significantly, the agreement also opens the door for India to store crude at Fujairah — ADNOC's primary export hub outside the Gulf — as part of India's own strategic reserve system. Holding reserves at Fujairah would give India rapid-access stocks positioned beyond the Hormuz chokepoint, a structural advantage no previous Indian SPR arrangement has attempted.

The IMEC promise and its headwinds

A more ambitious structural fix is embedded in the India-Middle East-Europe Economic Corridor (IMEC), the multimodal trade and energy infrastructure initiative announced at the G-20 in New Delhi in 2023.

Spanning approximately 6,400 km and connecting India's western ports — Mundra, Kandla, JNPA, and the under-construction Vadhavan Port — to the Arabian Gulf and onward overland to Europe, IMEC includes an explicit energy infrastructure pillar. Vadhavan alone, funded at ₹76,200 crore (US$8.58 billion), is expected to handle 23.2 million TEUs when complete.

But the Hormuz crisis also exposed IMEC's near-term limitations. Gulf port infrastructure, including facilities in the UAE, was directly targeted during the Iran conflict, casting doubt on how resilient any Gulf-transiting corridor can be during a West Asian military escalation. IMEC's northern connectivity also requires Israeli-Saudi normalisation that remains politically distant. The Centre for Social and Economic Progress notes that the corridor's 16th India-EU Summit endorsement in January 2026 and the Global Gateway alignment are positives, but implementation timelines remain ambitious and dependent on geopolitical conditions that are far from stable.

The Russian question after the truce

The return of Hormuz flows also revives a difficult calculation for India's oil ministry: what to do with Russian crude. During the crisis, Russia surged back to become the dominant supplier, with imports from Moscow rising sharply in May 2026 after having dropped to 1.15 million bpd in the first two months of the year from 1.7 million bpd through all of 2025.

The tightening of US sanctions on Rosneft and Lukoil in November 2025 and monthly rolling waivers for Indian imports have created a legal grey zone that Indian refiners navigate with increasing discomfort.

The ceasefire may have given the US leverage to press India harder on this front. The Atlantic Council piece linked the Hormuz crisis explicitly to a strategic opportunity for Washington to deepen energy ties with New Delhi by offering US LPG, crude, and LNG as a durable non-sanctioned alternative.

India signed its first structured US LPG contract earlier this year, covering an estimated 10% of domestic demand. With Hormuz reopening and the political case for Russian waivers weakening, the India-US energy relationship faces its most consequential test since the Ukraine-era price cap.

"The truce changes India's bargaining position with everyone — with Moscow, with Washington, with OPEC+," a New Delhi-based energy policy analyst said. "The question is whether Indian policymakers use this moment to lock in structural reforms or simply revert to the status quo ante. History suggests the latter is the more likely outcome."

What comes next: The reform agenda that cannot wait

Whether or not analysts' scepticism proves justified, the reform agenda that the Hormuz crisis has exposed is now on the table in a way it has not been for years. Five priorities stand out.

The first is SPR expansion. India's 9.5-day net import cover must rise significantly. The ADNOC deal at Chandikol and Visakhapatnam is a beginning; the government must follow through and accelerate Phase III of the SPR programme, which has been delayed since 2019. Storage at Fujairah offers an innovative offshore dimension, but domestic capacity remains the foundation.

The second is VLCC and deep-water port infrastructure. Mundra's January 2026 VLCC terminal is a genuine milestone, but India needs comparable infrastructure at other western coast ports to enable truly large non-Hormuz cargoes from West Africa and the Americas to discharge without logistical friction. The India Shipping News noted at the time that the Mundra terminal's pipeline link to Barmer is a template for integrated port-refinery connectivity that should be replicated.

Third, India needs a gas storage policy. The complete absence of strategic natural gas reserves is the most underappreciated gap in India's energy security architecture. The crisis revealed that LPG exposure — with 90% of imports transiting Hormuz — was in many ways more acute than the crude oil shock, and domestic alternatives are limited.

Fourth, the government should formalise and deepen the multi-supplier diversification strategy — Venezuela, Brazil, Guyana, West Africa — rather than treating it as a crisis-era workaround. India's refinery flexibility makes this economically viable; what is missing is long-term contract architecture and upstream equity investment commitments.

Fifth, and perhaps most counterintuitively, the post-truce environment is the right moment to begin an honest national conversation about the role of demand-side management in energy security. Solar, EV adoption, and efficiency improvements cannot substitute for crude oil in the short term, but they are the only instruments that reduce India's structural import dependence over the long term.

The morning-after test

The Hormuz ceasefire is unambiguously good news for India. It will ease freight costs, reduce inflation pressure, allow the government to reconsider petrol and diesel retail price adjustments, and restore supply comfort to refineries that have been running at elevated operational cost for three months.

But as one senior refinery sector executive put it: "Every time there's a crisis and then a resolution, we pat ourselves on the back for managing through it. What we never ask is why we had to manage at all."

The 2026 Hormuz crisis was the most severe test of India's energy security architecture in a generation. The country managed it — with improvisation, diplomatic flexibility, and considerable fiscal cost. Managing the aftermath, and using this rare window of political urgency to build a genuinely resilient energy supply system, is the harder and more important task ahead.