India’s electric vehicle transition is beginning to reshape the country’s industrial geography in ways that extend far beyond automobiles.

While headlines continue to focus on rising EV sales, subsidy debates and charging infrastructure gaps, a quieter transformation is unfolding across southern India, where a dense ecosystem of batteries, electronics, manufacturing, ports and clean-energy investments is gradually converging into what could become the country’s most important electric mobility corridor.

This shift may ultimately matter more than monthly vehicle registrations.

Over the past two years, Tamil Nadu, Karnataka, Telangana and Andhra Pradesh have steadily emerged as the preferred destinations for electric vehicle and battery-related investments. Unlike earlier phases of India’s EV transition, which revolved largely around consumer adoption and government incentives, the new phase appears increasingly driven by industrial clustering and supply-chain positioning.

Recent industry assessments suggest that southern states now account for a disproportionately large share of India’s EV manufacturing capacity, charging infrastructure deployment and battery ecosystem investments.

The rise of a southern EV corridor

The concentration is not accidental.

Tamil Nadu already possesses one of India’s deepest automotive supply chains, hosting major manufacturing facilities for Hyundai, Renault-Nissan, BMW and several component makers. Karnataka brings a strong electronics and software ecosystem to the table, while Telangana has aggressively marketed itself as a future hub for clean mobility and battery manufacturing. Andhra Pradesh, meanwhile, is leveraging port connectivity and industrial corridors to attract investments linked to exports and logistics.

Together, these states are beginning to form an integrated industrial region with characteristics increasingly similar to global EV manufacturing clusters seen in parts of China, Europe and the United States.

The implications extend well beyond the automobile sector itself.

Electric mobility is becoming deeply intertwined with batteries, semiconductors, electronics, grid infrastructure and renewable energy systems. This means the regions that dominate EV manufacturing may also gain influence over future clean-energy supply chains and industrial growth trajectories.

China’s rise in the global EV sector offers an important lesson here. The country’s dominance did not emerge solely because of vehicle manufacturing. It emerged because China built interconnected ecosystems involving battery firms, electronics suppliers, logistics infrastructure, mineral processing and export-oriented industrial clusters. India’s southern states now appear to be moving cautiously along a similar path.

Why batteries are becoming the real battleground

The growing strategic importance of batteries illustrates this transition particularly clearly.

Recent reports that Tata and JSW are exploring investments worth nearly US $1 billion in lithium iron phosphate (LFP) battery technology highlight how India’s EV ambitions are shifting towards localisation and chemistry control.

LFP batteries have become increasingly attractive globally because they are cheaper, thermally safer and less dependent on expensive nickel and cobalt supply chains. Chinese manufacturers, especially CATL and BYD, have expanded aggressively in this segment over the past few years, forcing competitors worldwide to reassess battery strategies.

India’s growing interest in LFP technology reflects a broader concern that future industrial competitiveness may depend less on assembling vehicles and more on controlling battery ecosystems.

This has important geopolitical dimensions.

The global EV industry is increasingly shaped by strategic competition over minerals, battery technologies and clean-energy supply chains. The United States and Europe are attempting to reduce dependence on Chinese battery dominance through subsidies and localisation policies. China, meanwhile, continues to strengthen its hold over processing and manufacturing networks linked to lithium, graphite and rare earth materials.

India finds itself navigating this increasingly fragmented global environment while trying to build its own manufacturing capabilities.

The recycling race begins

That challenge is partly why battery recycling is beginning to attract serious policy attention.

The recently announced India-European Union initiative on EV battery recycling technology reflects a growing recognition that recycling could become one of the defining industrial battlegrounds of the next decade.

Countries that establish large-scale battery recycling ecosystems early may eventually reduce their dependence on imported critical minerals while simultaneously creating domestic secondary supply chains for lithium, cobalt and nickel recovery.

This is particularly significant for India because the country remains heavily dependent on imports for many clean-energy technologies and raw materials. Several analysts believe that battery recycling could eventually evolve into a strategic industry comparable to semiconductor recovery and rare-earth processing.

“Battery recycling is not just an environmental issue anymore; it is becoming a strategic industrial capability,” said an executive at a Hyderabad-based clean-tech firm with knowledge of ongoing industry discussions. “Countries that recover materials domestically will have greater resilience against future supply shocks,” he added.

The risks beneath the momentum

Yet despite the optimism surrounding manufacturing and localisation, structural vulnerabilities remain visible beneath the surface.

India’s EV transition still depends heavily on imported cells, raw materials and specialised components. Much of the value addition within global EV supply chains continues to remain concentrated in East Asia, especially China. Building domestic capacity at scale will therefore require sustained investments not only in assembly plants but also in upstream supply chains, research capabilities and advanced manufacturing technologies.

There are also concerns that India could become overly dependent on a few regional clusters.

Southern India’s growing dominance in EV manufacturing may strengthen efficiency and ecosystem development, but it could also widen regional industrial imbalances if northern and eastern states fail to develop comparable capabilities.

Some analysts argue that India may eventually require multiple EV corridors distributed across different regions to avoid excessive concentration risks.

At the same time, the rapid rise of southern manufacturing hubs is reshaping investment patterns within India itself.

International firms increasingly view southern India as a stable base for export-oriented manufacturing and diversified supply chains. Toyota’s reported plans to expand assembly operations in India underline this growing perception.

Several multinational manufacturers are now reassessing their China exposure due to geopolitical tensions, trade restrictions and concerns over supply-chain concentration. India, particularly its southern states, is increasingly positioning itself as an alternative manufacturing destination within this evolving global landscape.

This trend may intensify further as Western countries seek to diversify clean-energy supply chains.

Yet India’s EV transition is likely to remain structurally different from those of Europe and North America in one crucial respect: affordability.

Unlike Western markets, where premium electric cars dominate public attention, India’s transition will likely continue to be driven primarily by two-wheelers, compact vehicles and commercial fleets. This could make India one of the world’s most important laboratories for low-cost electrification and mass-market mobility solutions.

The hidden challenge of logistics electrification

The freight sector may become particularly important in this context.

Recent industry discussions have increasingly highlighted logistics electrification as one of the least understood but most consequential parts of India’s EV transition.

While passenger EV adoption receives most public attention, freight transport consumes a far larger share of fuel and poses far greater electrification challenges. Commercial fleet operators require predictable charging access, lower downtime and reliable logistics infrastructure. Electrifying warehouses, transport corridors and fleet depots may, therefore, become as important as selling passenger cars.

This is where southern India may again gain an advantage.

The region’s port infrastructure, industrial parks and manufacturing ecosystems make it better positioned to integrate logistics electrification with export manufacturing and industrial corridors. If managed effectively, this could create powerful feedback loops between EV production, battery ecosystems and freight electrification.

Can infrastructure keep pace?

Charging infrastructure expansion remains uneven across the country despite rapid growth in installations. Industry estimates continue to suggest that charging deployment may struggle to keep pace with long-term EV growth projections.

Urban land constraints, distribution network pressures and financing challenges continue to affect infrastructure rollout in several cities. Delhi’s recent debates around transformer capacity, charging locations and urban integration challenges illustrate the complexities of scaling EV ecosystems beyond initial adoption phases.

At the same time, rising EV sales indicate that market momentum itself is unlikely to disappear anytime soon.

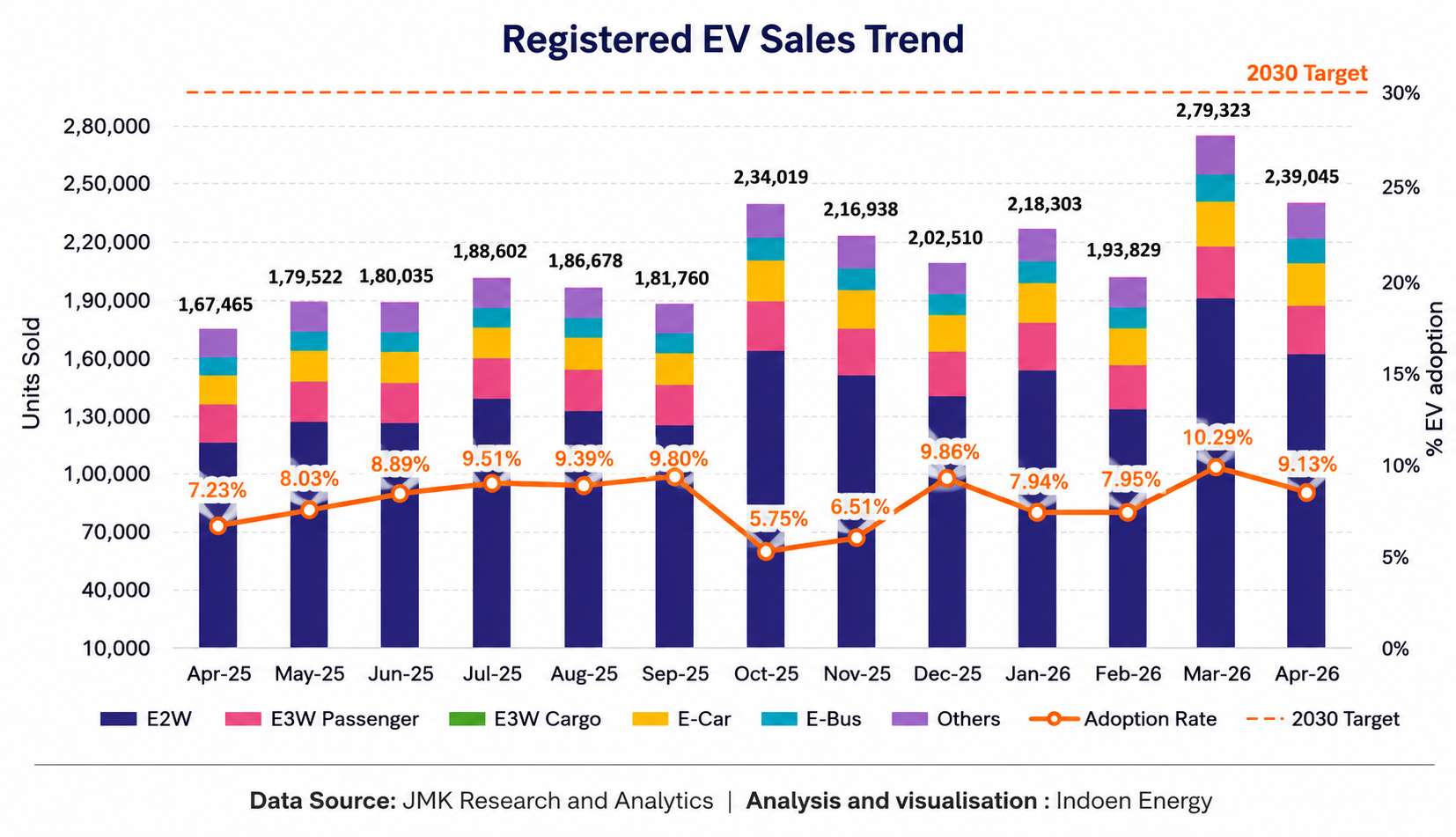

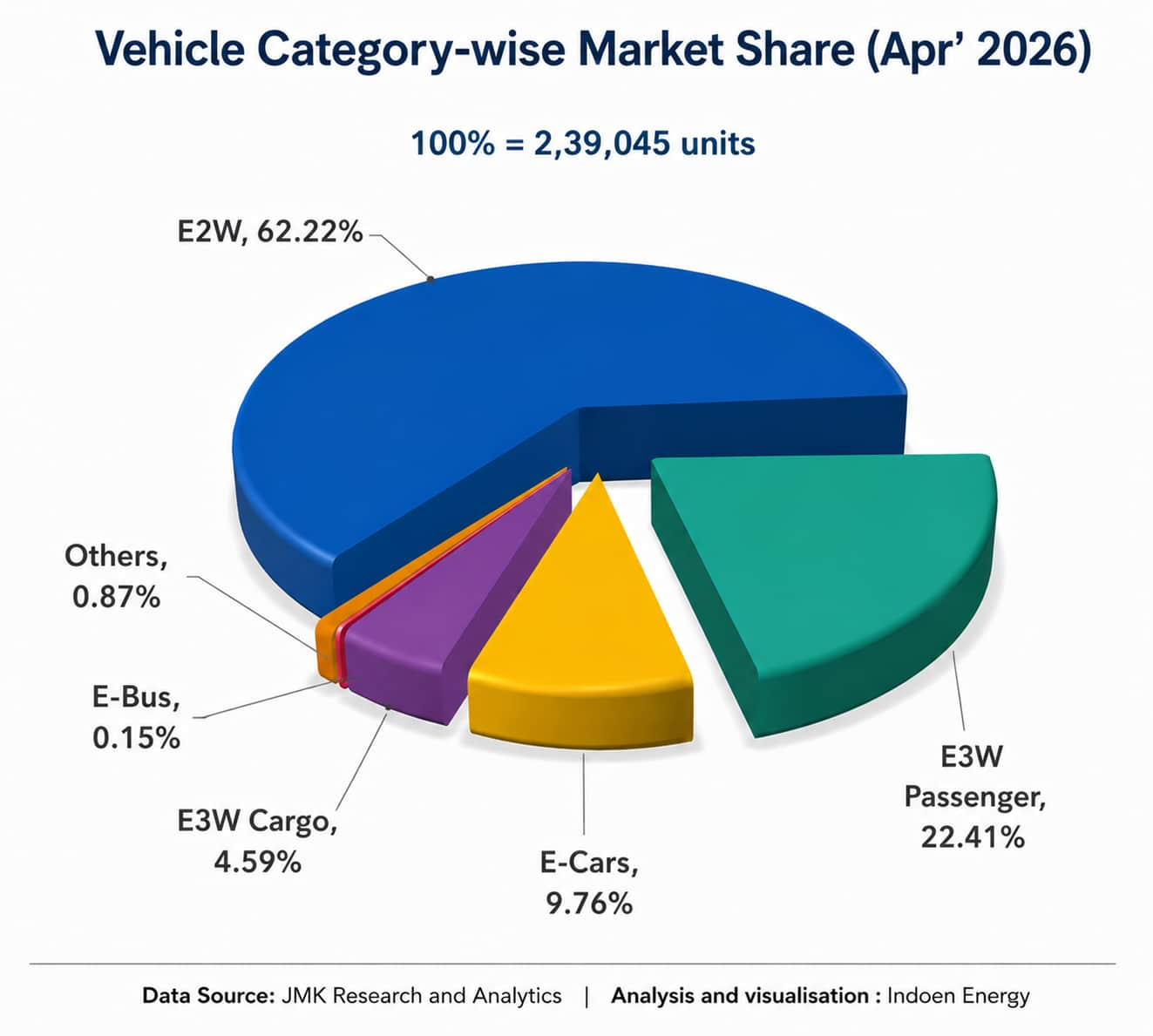

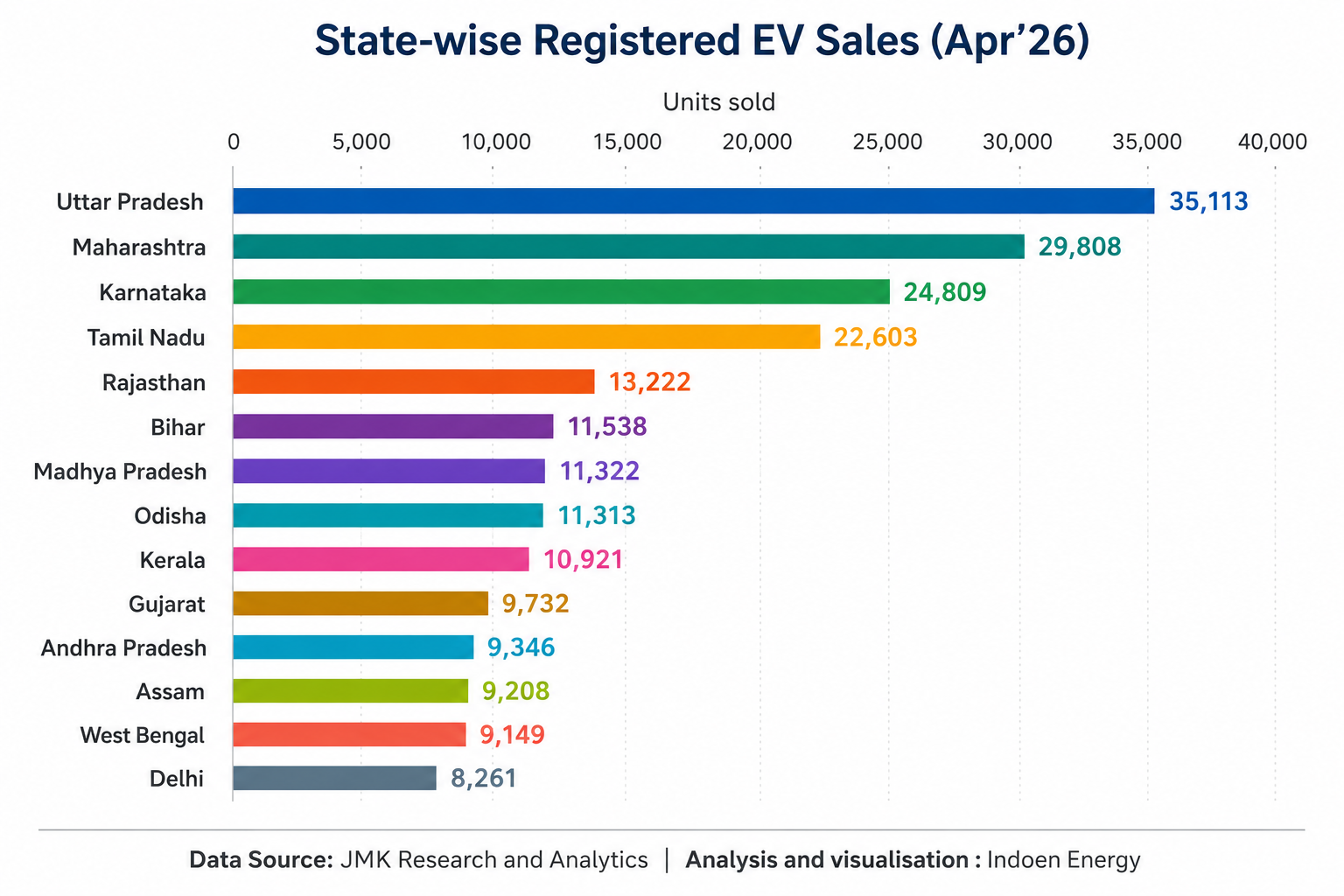

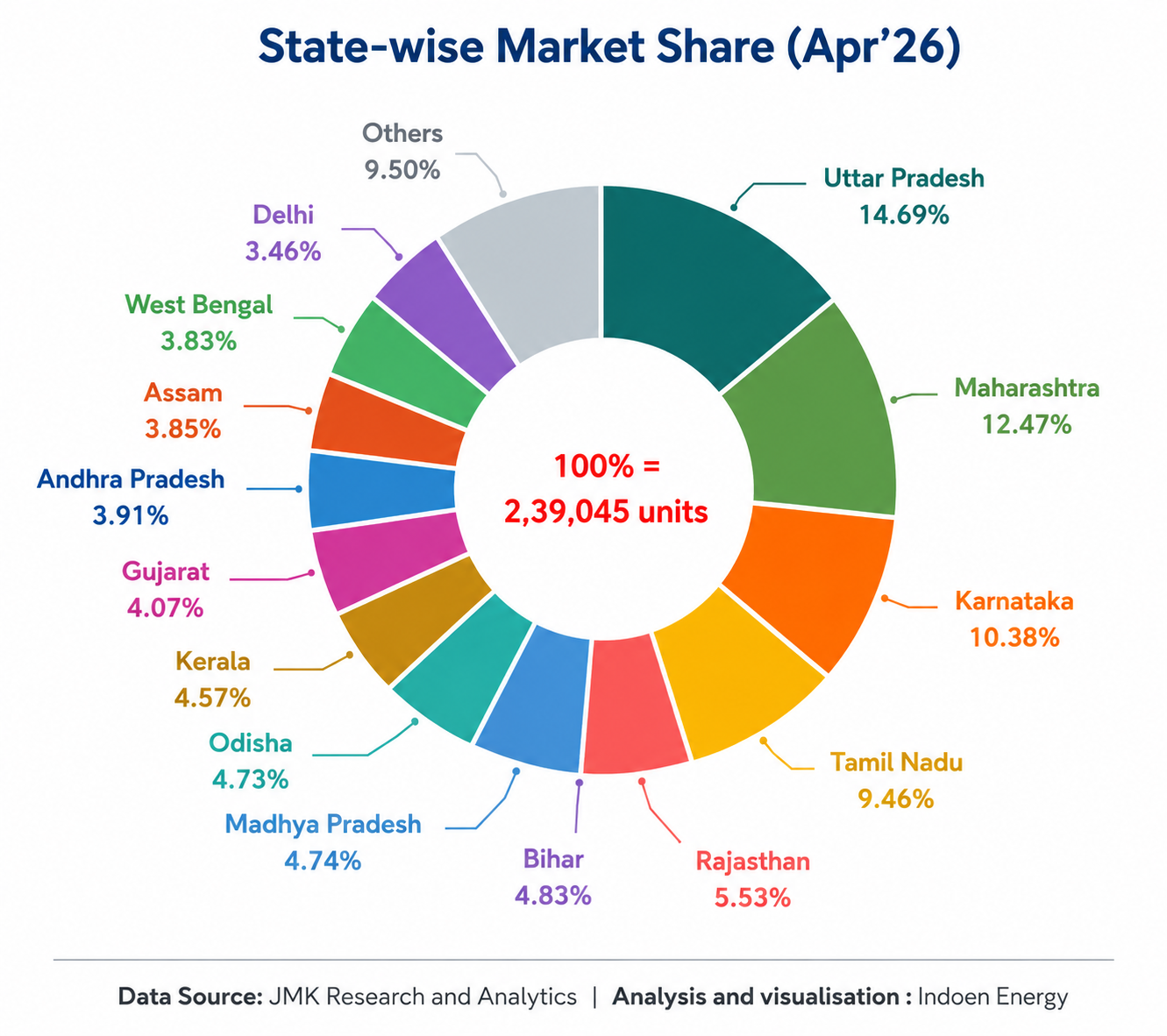

India’s passenger EV registrations reportedly rose sharply in April, reinforcing expectations that adoption will continue expanding despite infrastructure bottlenecks.

A new industrial geography is emerging. But the deeper story may no longer be about vehicle sales alone.

India’s EV transition is gradually becoming a contest over industrial geography, battery ecosystems and strategic supply chains. The regions that dominate these ecosystems may ultimately shape the country’s clean-energy economy for decades.

And at least for now, southern India appears to be moving ahead faster than the rest.