India's solar sector entered a new phase on June 1. A policy change that received relatively modest public attention could have far-reaching consequences for the country's renewable energy ambitions, manufacturing strategy, investment flows, and energy security.

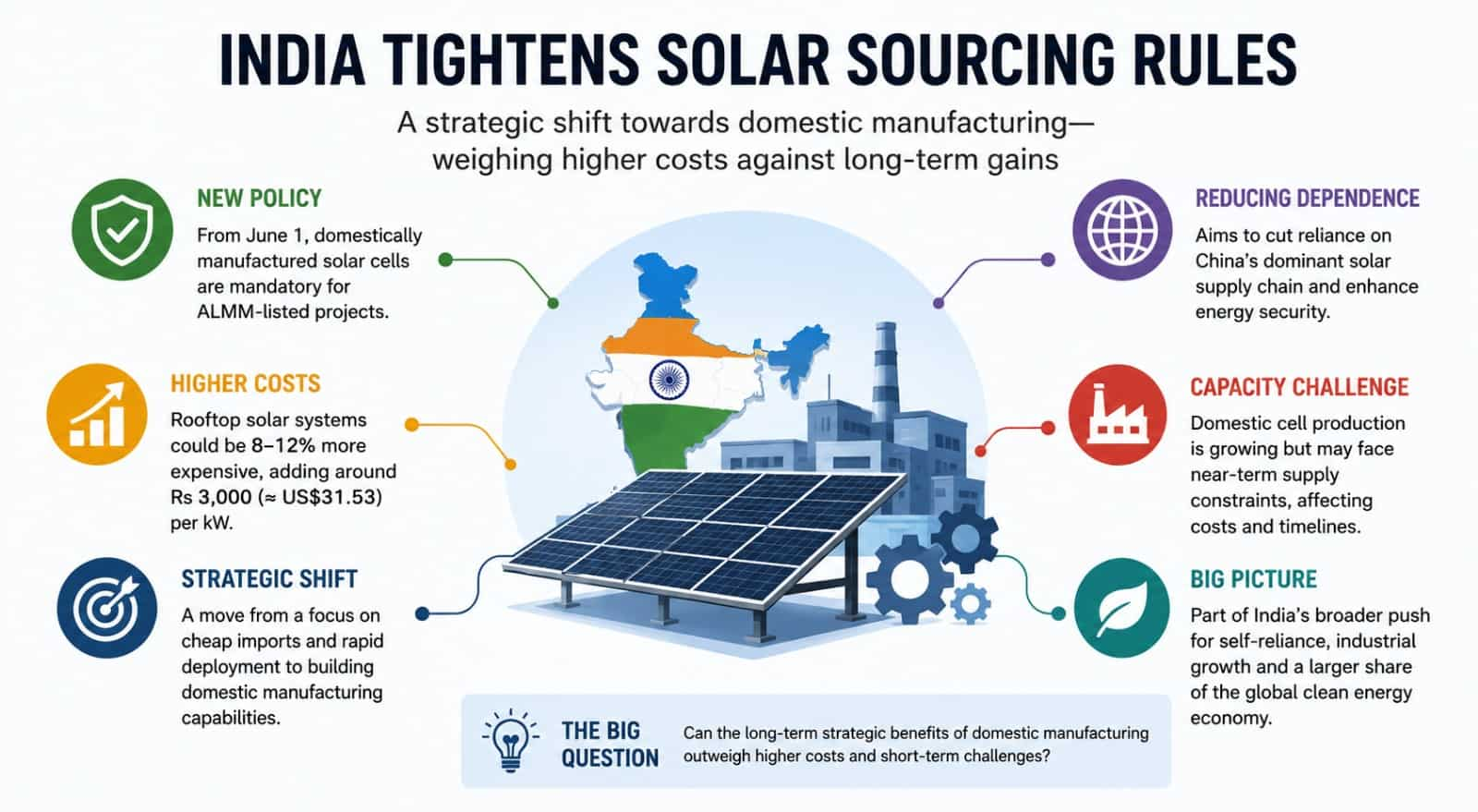

The government's decision to mandate the use of domestically manufactured solar cells for projects covered under the Approved List of Models and Manufacturers (ALMM) framework marks a significant shift in priorities. For more than a decade, India's solar expansion was largely built on one principle: deploy capacity as cheaply and rapidly as possible.

The latest rule change suggests that New Delhi is now willing to accept higher costs in the short term in pursuit of a broader strategic objective—building a domestic solar manufacturing ecosystem capable of competing with China.

The immediate concern is obvious. Industry estimates suggest rooftop solar systems could become 8-12% more expensive in the near term as developers switch from imported cells to locally produced alternatives. Some reports indicate that rooftop solar installations could become around Rs 3,000 (≈ US$31.53) per kilowatt more expensive, affecting residential consumers and commercial installations alike.

Yet focusing solely on rooftop costs risks missing the bigger story. India is attempting to reshape the economics of its solar industry.

A shift from deployment to industrial policy

For years, India's solar success story was inseparable from Chinese manufacturing. Cheap imported cells and modules enabled rapid capacity additions and helped India emerge as one of the world's fastest-growing solar markets.

According to industry estimates, China continues to dominate more than 80% of global solar manufacturing capacity across critical segments including polysilicon, wafers, cells and modules. While India has made progress in module manufacturing, dependence on imported upstream components remains substantial.

The June 1 rule effectively extends India's localisation efforts beyond solar modules to solar cells. The move follows earlier measures such as basic customs duties on solar imports and the Production Linked Incentive (PLI) scheme designed to encourage domestic manufacturing.

The policy reflects a broader industrial strategy visible across sectors ranging from semiconductors and batteries to electronics manufacturing. The objective is not merely energy generation but the creation of domestic industrial capabilities.

The China factor

The geopolitical dimension is impossible to ignore.

China's dominance in solar manufacturing has become one of the defining features of the global energy transition. Many countries pursuing renewable energy targets find themselves increasingly dependent on Chinese supply chains.

India's policymakers appear determined to avoid that outcome.

An interesting perspective comes from recent analysis examining how China views India's solar ambitions. For years, India was primarily seen as a major market for Chinese products. Increasingly, however, China may be viewing India as a potential competitor.

Indian companies including Tata Power Solar, Waaree Energies, Adani Solar, Vikram Solar and Reliance's clean energy ventures have announced substantial manufacturing investments. Several gigawatts of new cell and module manufacturing capacity are under development.

The strategic question is whether India can move beyond assembly and module manufacturing into higher-value segments such as wafers, ingots and eventually polysilicon.

The capacity challenge

The government's confidence in tighter sourcing rules is based partly on significant growth in domestic manufacturing capacity.

India's solar module manufacturing capacity has expanded rapidly over the past few years and now exceeds domestic demand in several estimates. Cell manufacturing, however, remains more constrained.

This creates a potential bottleneck.

Industry executives have warned that domestic cell production may struggle to fully meet near-term demand from utility-scale and distributed solar projects. If supply constraints emerge, project costs could rise and commissioning schedules could face delays.

This creates an interesting contradiction at the heart of India's energy transition.

The country wants to accelerate renewable energy deployment while simultaneously reducing import dependence. Achieving both objectives at the same pace may prove difficult.

The challenge becomes particularly important given India's target of reaching 500 GW of non-fossil fuel capacity by 2030.

The hidden battle upstream

Perhaps the most important and least discussed aspect of the policy is what comes next.

The current focus is on solar cells. However, cells themselves depend on wafers, which depend on ingots, which depend on polysilicon. China remains overwhelmingly dominant in these upstream segments.

In many ways, India's solar challenge today resembles the situation faced by other strategic industries. Manufacturing modules and assembling final products is relatively easier. Building complete supply chains is significantly more difficult.

This is where the next phase of policy intervention is likely to emerge.

Several analysts expect future government measures to increasingly focus on upstream manufacturing, particularly as India seeks to reduce vulnerabilities associated with external supply chains.

If successful, India could become one of the few countries outside China with a relatively integrated solar manufacturing ecosystem.

Global lessons and cautionary tales

India is not alone in pursuing localisation.

The United States has used tax credits and manufacturing incentives under the Inflation Reduction Act to stimulate domestic clean energy production. Europe is debating similar strategies amid concerns about industrial competitiveness and strategic dependence.

However, international experience also highlights risks.

Protectionist measures can raise costs for consumers and developers if domestic industries fail to scale quickly. Excessive localisation requirements can sometimes slow deployment and undermine renewable energy targets.

India therefore faces a delicate balancing act.

Move too slowly on localisation and dependence on imports continues. Move too aggressively and solar deployment costs rise, potentially affecting adoption rates.

A trillion-dollar question

The broader significance of the June 1 rule extends beyond solar panels.

Global investment in clean energy exceeded US$2 trillion in 2024 according to international estimates. Much of that spending is increasingly tied to industrial policy, manufacturing competitiveness and supply chain security rather than simply emissions reduction.

India's latest solar rules signal that New Delhi wants a larger share of that economic opportunity.

The real question is whether consumers, developers and investors are willing to absorb short-term costs in exchange for long-term strategic gains.

That debate is likely to define not only India's solar sector but much of its wider energy transition over the coming decade.

A decade ago, the central challenge was deploying solar power cheaply. Today, the challenge is building an entire industrial ecosystem around it.

The June 1 policy change suggests India believes the second challenge may now be just as important as the first.