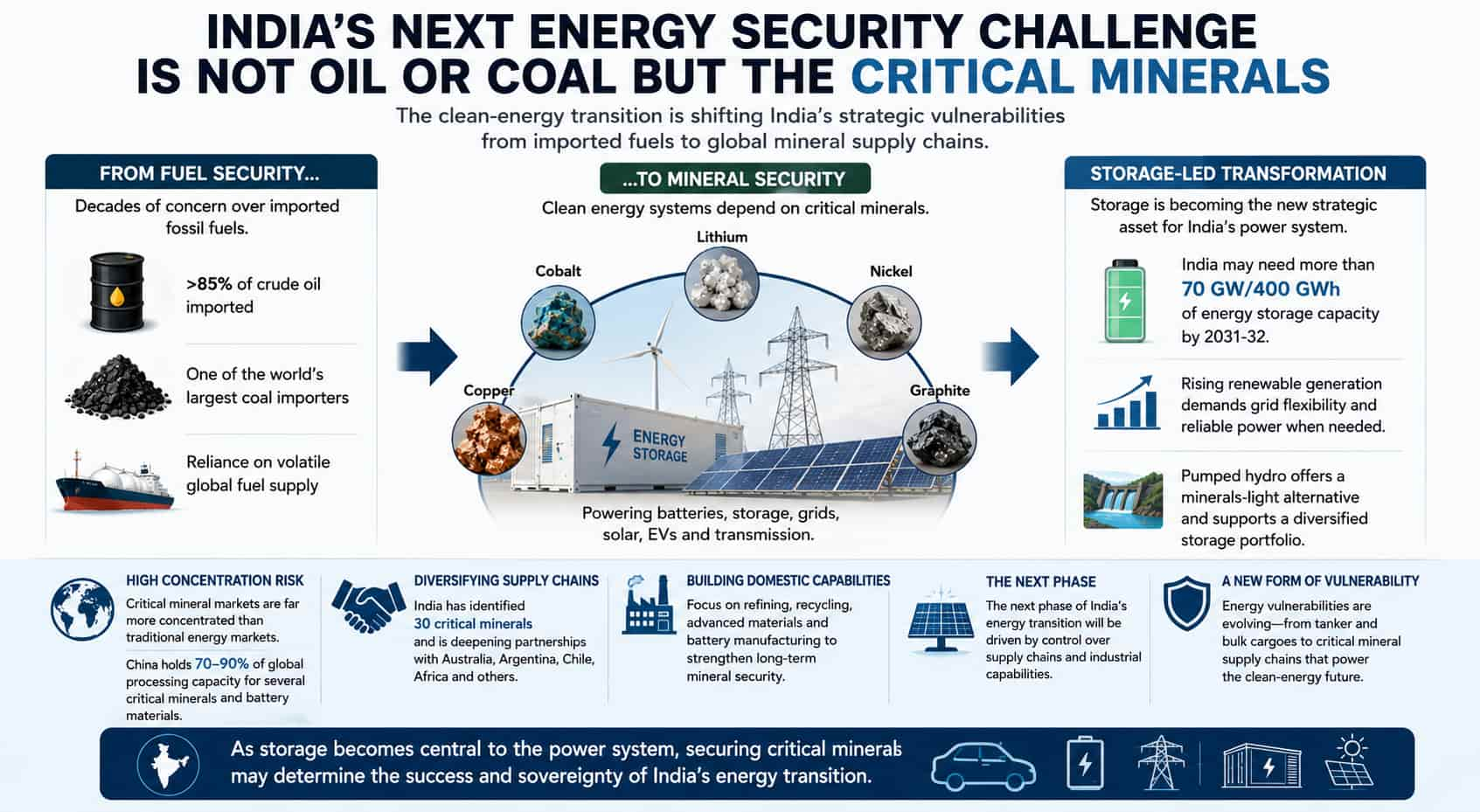

For decades, India's energy security strategy revolved around a familiar set of concerns. Would crude oil shipments continue to flow through increasingly volatile geopolitical corridors? Could coal imports remain affordable during periods of international market disruption? Would liquefied natural gas supplies remain available during global energy crises?

As India accelerates its clean energy transition and prepares for a storage-led transformation of its electricity sector, policymakers are confronting a different challenge: securing access not to fuels, but to the minerals that will underpin the next generation of energy infrastructure.

The transition is changing the very meaning of energy security.

Recent analysis from the Institute for Energy Economics and Financial Analysis (IEEFA) highlights how India's imports of critical minerals such as lithium, cobalt, nickel, graphite and copper remain heavily concentrated among a relatively small group of supplier countries.

At the same time, industry experts argue that India's power market is entering a phase where energy storage, rather than generation capacity alone, will determine the flexibility and resilience of the electricity system.

The convergence of these two trends could shape India's energy future far more profoundly than many investors currently appreciate.

From fuel security to mineral security

India's traditional energy-security concerns were rooted in fossil fuels.

The country imports more than 85% of its crude oil requirements and remains one of the world's largest coal importers despite substantial domestic reserves. Policymakers spent decades building strategic petroleum reserves, diversifying import partners and securing long-term supply arrangements.

However, the technologies expected to dominate future energy systems depend on a very different set of resources.

Solar modules require substantial quantities of copper and specialised materials. Electric vehicles rely on battery minerals. Grid-scale storage systems depend on lithium, graphite, nickel and cobalt. Transmission infrastructure requires significant volumes of copper and aluminium.

As a result, India's energy transition is increasingly becoming a minerals story.

According to IEEFA, India remains almost entirely import-dependent for lithium, cobalt and nickel. Chile has emerged as India's largest supplier of critical minerals, while China continues to occupy a systemically important position across several mineral value chains. Between FY2019 and FY2025, India imported approximately 2.8 million tonnes of critical minerals from Chile, largely driven by copper ore imports.

Storage becomes the new strategic asset

The timing is significant because India's electricity system is entering a phase where storage is becoming increasingly important.

For years, the focus of India's renewable-energy expansion was generation capacity. Solar and wind projects delivered dramatic cost reductions and rapidly expanded installed capacity. Yet as renewable penetration increases, a new challenge has emerged: matching electricity supply with demand throughout the day.

Industry participants increasingly describe storage as the next critical layer of infrastructure.

According to market experts, India's electricity sector is entering a ‘storage-led transformation phase’ as rising renewable generation exposes gaps in grid flexibility. The constraint is no longer merely producing electricity but ensuring that electricity is available when consumers need it.

India's storage ambitions are also substantial. The Central Electricity Authority estimates that India could require more than 70 GW/400 GWh of energy storage capacity by 2031-32 to support renewable integration and maintain grid stability.

Battery energy storage systems, pumped hydro projects and hybrid renewable-storage projects are therefore attracting growing attention from utilities, developers and investors.

That creates a paradox. The technologies intended to improve India's energy independence may simultaneously deepen dependence on overseas mineral supply chains.

A vulnerability the world is only beginning to understand

The issue extends well beyond India. The International Energy Agency has repeatedly warned that critical-mineral markets remain significantly more concentrated than traditional energy markets. In several minerals, the top three producing or processing countries account for the overwhelming majority of global supply.

One of the more surprising developments is that concentration is often greater in refining than in mining.

China today accounts for roughly 70-90% of global processing capacity for several critical minerals and battery materials, giving it a pivotal position in global clean-energy supply chains.

The lesson was reinforced during the pandemic-era semiconductor shortages and Europe's gas crisis following Russia's invasion of Ukraine.

Energy transitions do not eliminate supply-chain vulnerabilities. They often relocate them.

India's diversification strategy gathers pace

India is not standing still. The government has identified 30 critical minerals as strategically important and has accelerated efforts to secure overseas resources, promote domestic exploration and strengthen international partnerships.

India has expanded engagement with Australia, Argentina, Chile and several African nations as part of a broader effort to diversify supply sources and reduce concentration risk.

The strategy reflects a growing recognition that mineral security is becoming inseparable from industrial competitiveness.

The challenge is not merely ensuring sufficient imports. It is also about developing domestic capabilities in refining, recycling, advanced materials and battery manufacturing.

This helps explain why governments worldwide are increasingly competing for investment across entire critical-mineral value chains rather than focusing solely on mining projects.

The overlooked role of pumped hydro

An interesting counterpoint to the battery narrative is the resurgence of pumped hydro storage.

Much of the global conversation around storage focuses on batteries. Yet pumped hydro offers an alternative pathway that relies more heavily on engineering and geography than imported minerals.

India currently has a large pipeline of pumped hydro projects under development, reflecting growing recognition that storage diversification can also strengthen energy security.

This may become one of the most important strategic choices facing the power sector.

Rather than relying overwhelmingly on one storage technology, India could reduce future supply-chain risks by building a more diversified storage portfolio.

The next phase of the energy transition

The first phase of India's clean-energy transformation was driven by falling solar costs. The next phase may be driven by something far less visible: control over supply chains. This is the real significance of the emerging storage economy.

The debate is no longer simply about how many gigawatts of renewable energy India can install. It is increasingly about whether the country can secure the minerals, technologies and industrial capabilities needed to support a low-carbon economy at scale.

That represents a profound shift in the concept of energy security. For most of the past half-century, India's energy vulnerabilities arrived by tanker and bulk carrier. In the decades ahead, they may arrive through mineral supply chains.

And as storage becomes central to the power system, the countries that control those supply chains could exert influence comparable to that once held by the world's major oil producers.

Follow us on : X | LinkedIn | Facebook | Bluesky